Big Themes for 2025: Energy Scenario Normalization, Power Surge, Technology-Driven Growth

Navigating the Energy Macro

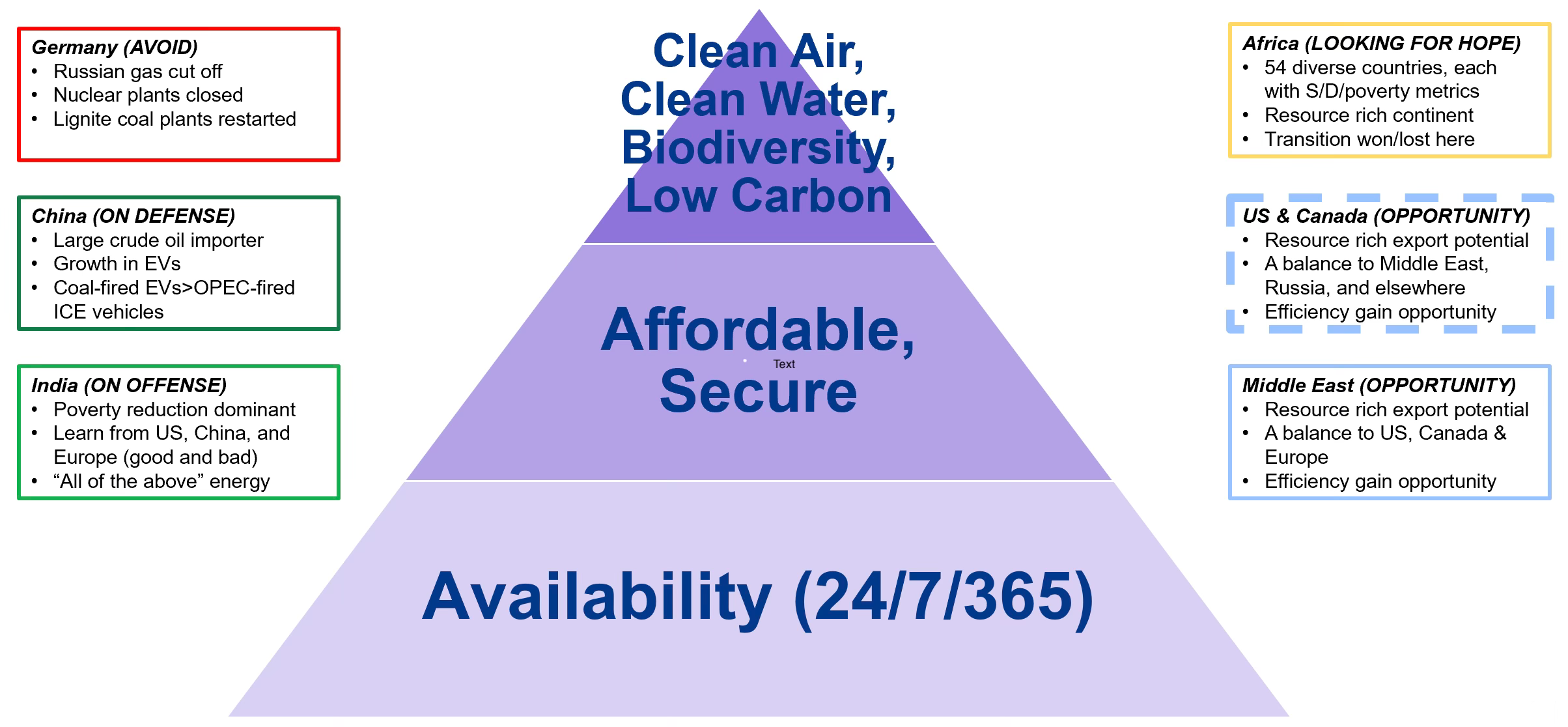

As we start 2025, we are filled with a renewed optimism about the fundamental outlook for the broad energy sector, including traditional oil & gas, power, and select new energy sources and technologies. The Energy TransitionTM era—i.e., the narrow definition which treated achieving net zero carbon emissions as the priority objective—decisively ended in 2024. Policy makers, investors, and industry executives are recognizing the urgent need to turn back to what energy has always been about: abundance and reliability as the priorities followed closely by affordability and geopolitical security. Environmental and climate considerations will remain an important part of the conversation but no longer dominate the narrative in what was a perverse inversion of energy’s hierarchy of needs (Exhibit 1). We say goodbye and good riddance to the failed “climate-is-all-that-matters” ideology of the last 5-6 years.

Exhibit 1: Energy scenarios are on-track to return to reflecting the traditional hierarchy of needs, not the inversion that was forced on the world over the past 5-6 years

Source: Veriten.

The biggest themes we see for 2025 are as follows:

Energy Scenario Normalization: Net zero is fading fast as the defining energy scenario narrative. Countries will solve for reliability, affordability, and geopolitical security first and foremost, which, paradoxically in our view, will eventually spur broad-based decarbonization as billion-person-scale economies seek energy sources and technologies that they can control.

Power Surge: Power has become arguably the super-cycle growth opportunity in energy. In the 2000s, it was the emergence of China and the BRICs that drove energy. The power growth opportunity is being driven by (1) the combination of aging power infrastructure, the growing share of intermittent resources, and premature retirement of dispatchable power sources in developed economies; (2) rising energy demand in developing countries; and (3) and the turbocharging of demand growth in both developed and developing regions due to aggressive data center growth. In our view, there is no one-size-fits-all approach, business model, or opportunity set to take advantage of a power market super-cycle.

Energy Sources and Technologies: We see natural gas as a big winner of the shift away from The Energy TransitionTM coupled with a power super-cycle. We also anticipate continued robust growth in solar, which in some respects has been overly categorized as a “climate action” energy source. Solar has a number of positive attributes around geopolitical security and modularity that we see as more important to its continued growth than necessarily its low-carbon attributes. Both natural gas and solar are likely to be big winners in a power super cycle. As broad-based solutions to meeting future energy needs, we are less enthusiastic about Big Wind and hydrogen (niche opportunities might exist for both). In terms of future areas to watch, nuclear is clearly gaining momentum and we are open-minded to evaluating the potential for geothermal and long-duration battery storage economics to eventually prove viable at a large scale. The future role of coal is hotly debated. Thus far, its death has been greatly exaggerated. In our view, continued coal growth in developing economies seems inevitable until an alternative base-load/dispatchable energy becomes economically competitive.

We have long expected EVs (electric vehicles) to experience significant, long-term growth, but fall well short of the aggressive “hockey stick” forecasts that were touted just a few years ago and called for near 100% EV penetration at some point in the 2030s. In our view, signs of progress on autonomous driving could be the key to a more significant disruption to transportation markets. That said, it is too early to have strong views on what that would mean for EV versus ICE (internal combustion engine) growth, miles driven by technology, and therefore gasoline and electricity demand.

Energy Scenarios Normalization

The 2021-2024 period of high-profile energy scenarios that obsessively and inexplicably only toggled between various “net zero” alternatives will be remembered as among the most ridiculous and damaging for countries and companies. The scenarios were aided and abetted by the similarly disgraceful “net zero” banking alliances ring-mastered by the Glasgow Financial Alliance for Net Zero (GFANZ) and its offshoots the Net Zero Banking Alliance (NZBA) and Net Zero Insurance Alliance (NZIA). Thankfully, the Net Zero Industrial Complex is being relegated to the dustbin of history.

The International Energy Agency (IEA) takes much of the slings and arrows for its infamous Net Zero by 2050 report originally published in May 2021. We have strongly argued against its key assumptions from Day 1, and it was a contributing motivator to our creating Super-Spiked in November 2021 and un-retiring to Veriten in March 2023. Incredibly, it also served as an apparent inspiration for many similar forecasts from large European oil companies. We recognize that societal pressure to go along and get along with the net zero obsession was significantly greater in Europe than in the United States, and that the senior leadership at some of these companies seemed to sincerely believe in their scenarios as exemplified by corporate actions and high-profile “transition” strategies.

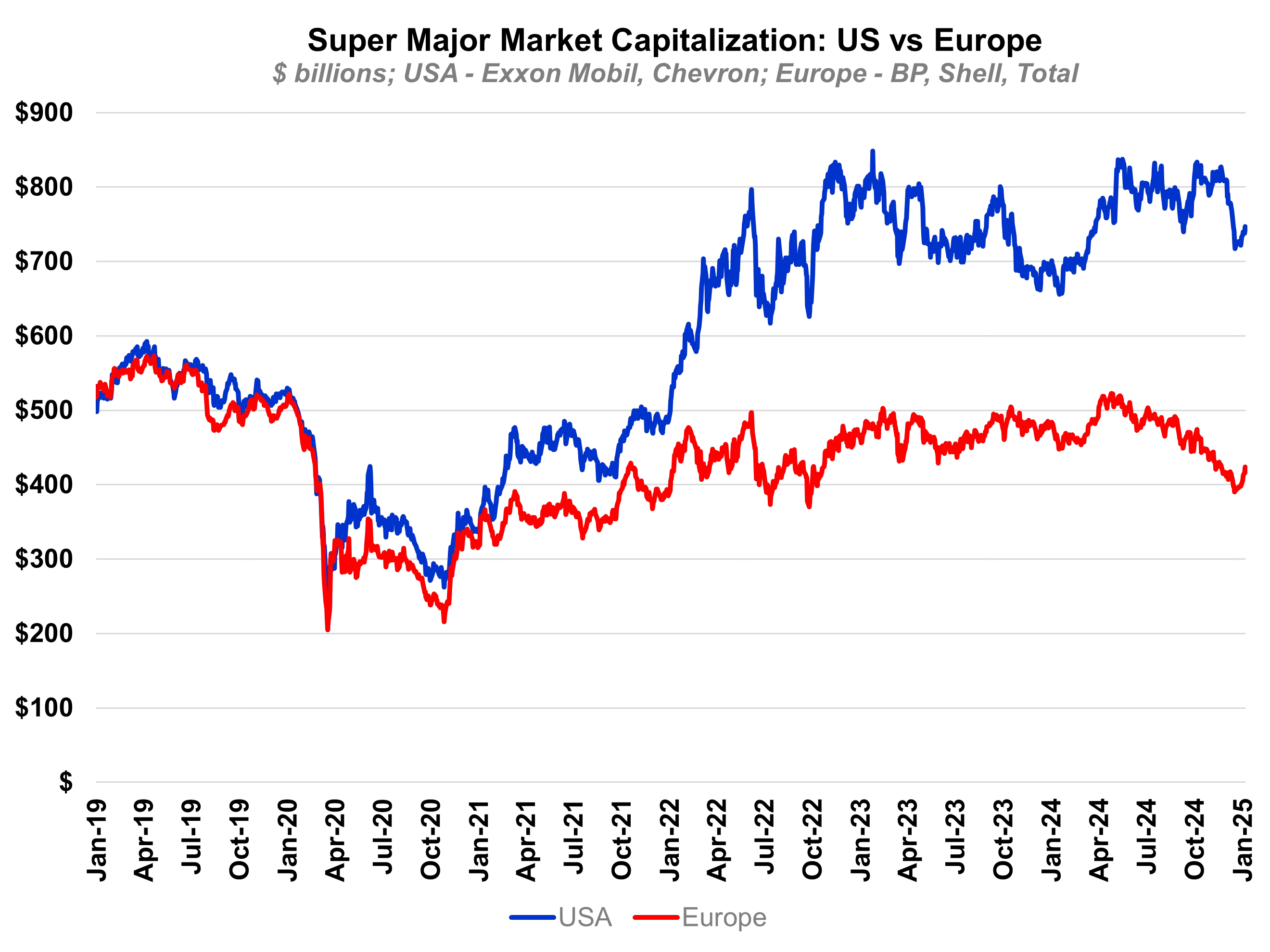

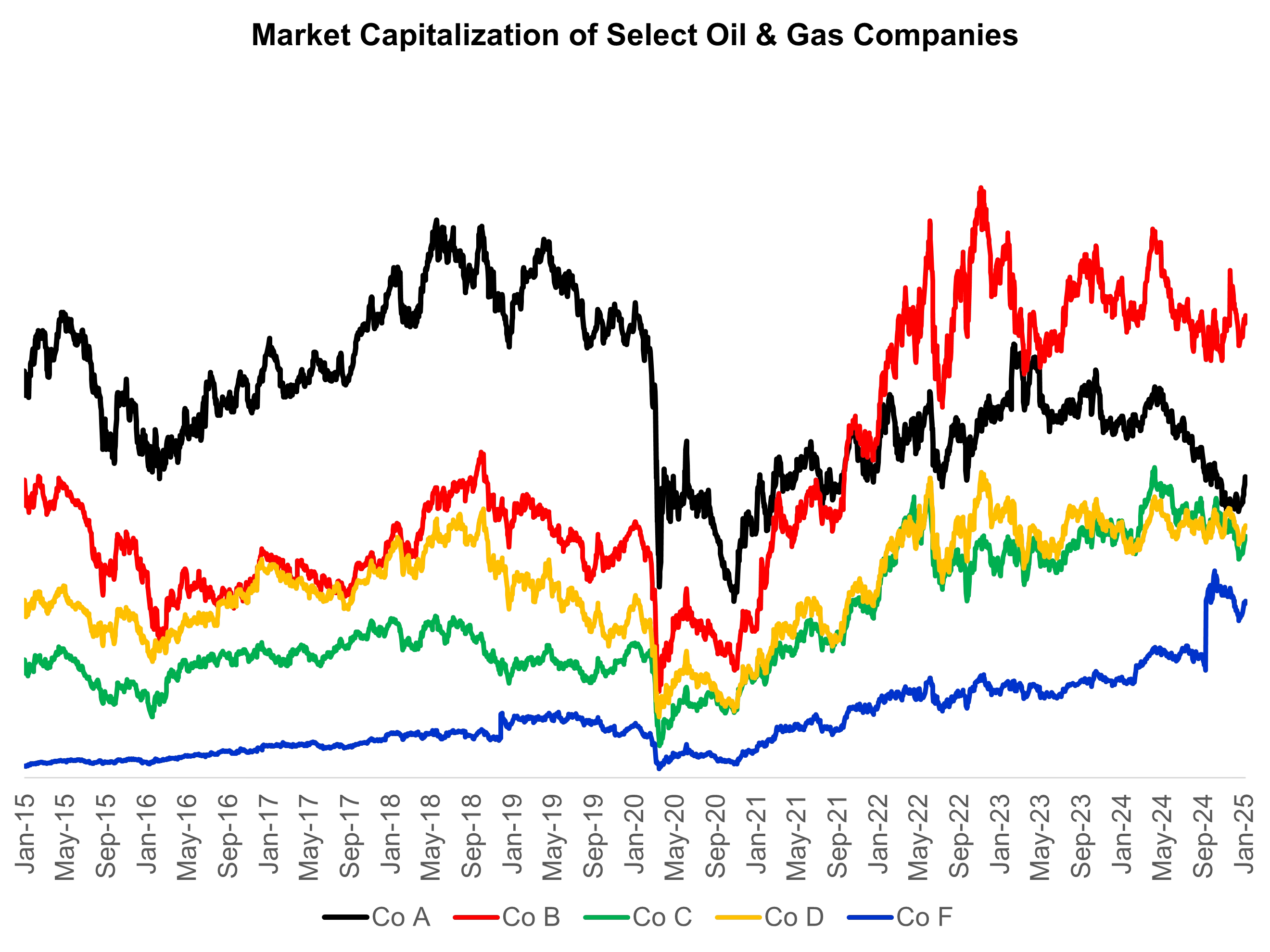

However, the outperformance of US oil and gas firms, both large and even medium sized, versus the biggest net zero believers among European large-cap oils has been staggering (Exhibits 2 and 3). It has unsurprisingly led to a retreat away from the most aggressive transition strategies by those same European Big Oils. We also recognize there has been well-received leadership changes at some of those companies that point to a brighter future going forward.

Both countries and companies need realistic and pragmatic energy scenarios that can underpin economic progress and on which to base corporate strategy. Political correctness, climate virtue signaling, and the fashion-of-the-day have no role to play in long-term strategy or economic planning.

Exhibit 2: US Super Majors have outperformed Europeans during The Energy TransitionTM era

Source: Bloomberg, Veriten.

Exhibit 3: A quartet of US E&Ps (Companies B, C, D, and F) have dramatically outperformed a European oil (Company A) with an aggressive transition strategy

Source: Bloomberg, Veriten.

Power Surge: This generation’s energy super-cycle

We increasingly see meeting the world’s power needs as this generation’s energy super-cycle. Twenty years ago it was the rise of China and the BRICs that turbocharged GDP growth, in particular for crude oil, copper, and other commodities used to fuel transportation, property and infrastructure growth. The commodities, energy sources, and technologies that drive global power are not identical to what mattered most for the China/BRICs expansion.

A few thoughts on this topic:

US merchant power companies (as well as traditional utilities) are already a well-known winner of this trend (Exhibit 4). But that does not mean everyone needs to become a merchant power producer.

There are clearly various equipment and service providers that will benefit from rising power demand and related infrastructure needs (e.g., transmission lines, turbines, etc.).

The opportunity to meet the power needs of technology, data center, and industrial companies opens up new business model opportunities for traditional energy and power producers as well as new companies in new business lines.

For oil and gas producers that rightfully view their companies as being focused on “molecules” rather than “electrons,” it will likely take some creativity, risk-taking, new skillsets, and new executives to figure out how and where to get involved in power markets, if at all. Let us be clear on that last point: it will not make sense for every company to pursue power market opportunities. It does make sense to understand the spectrum of opportunities and macro implications.

How companies are capitalized, whether they are wholly-owned or joint ventures, and the opportunity for M&A versus organic CAPEX are among the many considerations companies will need to work through.

Profitability in the power sector will be less about a price-driven super-cycle as one would see in say crude oil or copper markets than it will be about helping companies and countries meet power needs at a price and cost structure that can yield a competitive, levered rate of return on the capital invested. To be clear, price and market signals remain highly relevant; it’s just that the nature of it is different than in a pure commodity market like crude oil. Working through different layers of regulation and market structures is a needed skillset and area of expertise that matters more in the power market than say being a West Texas oil producer.

Exhibit 4: US merchant power producers have become stock market darlings

Source: Bloomberg.

Energy Sources and Technologies

The biggest and most obvious winners in terms of energy sources are natural gas and solar. Natural gas we see as a critical future fuel and should have long ago shed its “transition fuel” moniker. Solar has similarly been viewed as a “climate action” renewable, low-carbon energy source. While it is low-carbon and mostly renewable (solar panels don’t last forever), we see it as key to geopolitical security and flexibility for many countries and companies. Like natural gas, we believe solar ought to also be rebranded as a critical energy source.

Key positives of natural gas:

The resource opportunity in friendly areas is massive and low-cost in nature.

It can be used for dispatchable base-load or peaking power generation.

While there will be occasional increases in the price of natural gas in competitive supply markets like the United States, we do not believe high prices will prove sustainable given the abundance of the resource.

The main negative of natural gas is that while it can be shipped anywhere, the cost to doing so is not trivial and can make imported LNG (liquefied natural gas) uncompetitive with domestic base-load alternatives such as coal. We believe climate concerns about methane emissions are an issue that is on-track to be addressed. However urgent or not one feels about climate change risks, there is zero reason to waste a valuable resource like methane when so much of the world remains energy poor.

Key positives of solar:

Once installed, it is a de facto zero variable cost, domestic resource and source of geopolitical security since the sun does not need to be imported from foreign adversaries or supposedly friendly countries that threaten export halts (e.g., a permit pause).

It is modular in nature and can be scaled down or up to meet a variety of needs. As an example, individual homeowners can pair solar panels on their roof with battery storage to meet their energy needs. Practically speaking, a homeowner cannot have their own natural gas, nuclear, or coal plant. A similar reality exists for many businesses.

The key negative of solar is of course that it is intermittent in nature, not every region enjoys the same degree of solar radiation, and the cost of firming up solar power can be significant. Similar to natural gas executives that should stop reenforcing “transition fuel” narratives, solar value-chain companies we think would benefit from shedding the perception that the only reason to use solar is to fight climate change. That is no longer true and undermines the all-in value of the solar industry. That said, if solar truly is cost competitive, it ought not to need ongoing subsidies.

In terms of other energy sources and technologies, we would make the following observations:

Nuclear (bullish): Gaining significant momentum as a viable, long-term source of base-load, zero carbon power.

Geothermal and long-duration battery storage (worth studying): We are open minded about the potential for geothermal and long-duration battery storage to gain share and benefit from improved economics in the years ahead. Both are areas we need to dive deeper into.

Big Wind (bearish): In our view, Big Wind does not enjoy the same positives as solar in particular in terms of modularity. We would note that there are some newer wind companies that we would not categorize as “Big Wind” that are seeking to provide new solutions for homes and businesses that we are not referring to in this discussion.

Hydrogen (over-hyped): We have long been highly skeptical that hydrogen, in particular the “green” variety, will prove to be a large-scale alternative to crude oil- or natural gas-based fuels. Hydrogen is appropriate in various niches.

Coal (its death has been greatly exaggerated): Is “clean coal” a thing? Can it become a thing? Coal demand is going to grow regardless. Instead of pretending that global demand declines are imminent, what can be done to reduce its overall environmental impact?

EVs: Progress on autonomous driving is likely the key enabler to broader penetration of the global transportation fleet. We are watching this area closely and believe the ultimate impact on oil and electricity demand is uncertain at this time.

Other themes for 2025

Other themes that we expect to expand upon in future posts include:

Crude Oil: 2025 may be the last big bump for non-OPEC growth for some time, with both US shale oil and Brazil expected to mature and slow. That said, we remain in the Super Vol rather than super-cycle camp at this time owing to the lackluster global GDP backdrop. A more meaningful pick up in global GDP growth consistent with a return to closer to +1.5 mn b/d of annual demand growth is an important catalyst to believing a stronger upcycle would be at hand.

China: With oil demand expectations sufficiently lowered, China looks to be on-track to transition to being merely another important, but no longer decisive, country for oil markets. The China slowdown is otherwise a near-term headwind for crude oil markets.

M&A: Traditional energy sector consolidation continues, especially if a Super Vol rather than super-cycle commodity macro backdrop persists. The degree to which power market opportunities play into traditional energy sector M&A will be an area to watch.

US/Canada Energy Dominance: We admit to feeling a high degree of excitement that the incoming Trump Administration along with a change away from the Trudeau regime in Canada in 2025 can spur a return to “all of the above” energy sensibilities, a point that was bi-partisan in the U.S. prior to 2016 before the rise of “climate-is-all-that-matters” religiosity. America and Canada Energy Dominance would support maximizing long-term crude oil and natural gas/LNG production from the massive resource base that exists in both countries. Especially since the world is again remembering energy’s true hierarchy of needs (abundance and reliability come first followed by affordability and geopolitical security). It would also include reforming the ill-named Inflation Reduction Act (IRA) in the United States to support domestic new energies developments, but in a manner that is technology agnostic (i.e., without explicit or implicit mandates) and not dependent on perpetual subsidies for uneconomic technologies.

⚡️On A Personal Note: A 25-Year Career and Life Lookback

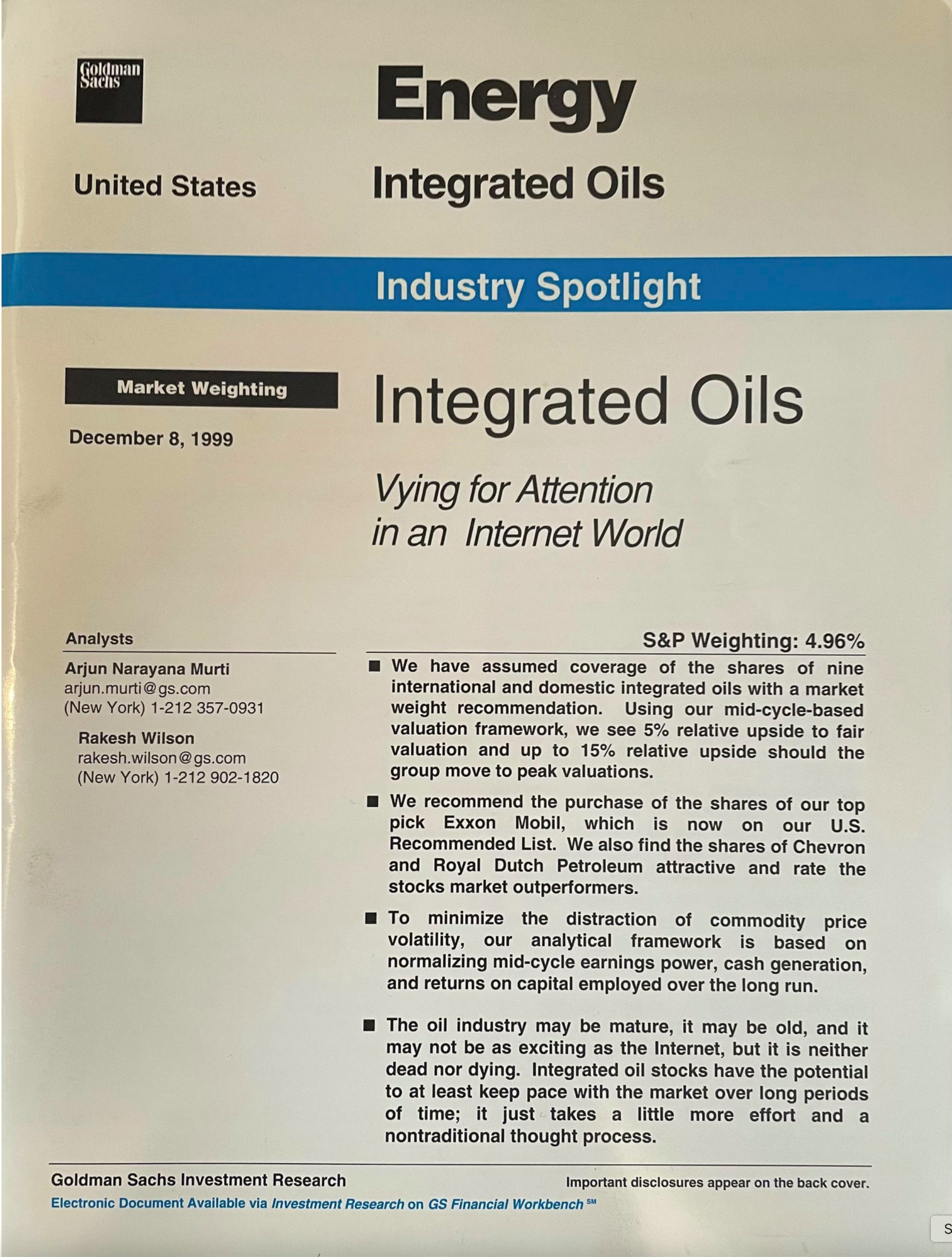

Earlier this week my friend and former colleague Brian Singer reminded me at the 2025 Goldman Sachs Energy, Clean Tech & Utilities conference in Miami that we were just a few weeks past the 25-year anniversary of my initiation report at Goldman Sachs, Vying for Attention In An Internet World. Yes, we have had periods of great enthusiasm for the technology sector and a corresponding complete lack of interest in traditional energy before. Little did I know then that I would be just five years away from a career-defining Super-Spike call that is the namesake for this publication.

Exhibit 5: Our Goldman Sachs launch report

Source: Goldman, Sachs & Co.

Notably, my wife and I were married the same week I launched coverage, arguably a coincident timing that probably should not be considered a best practice. If I am remembering correctly, we were waiting for the Exxon-Mobil merger to close which pushed the dates together. In recognition of these dual, notable 25-year anniversaries—and in the spirit of reflecting on the successes and areas for improvement in my life and career—here is a “best of/worst of” look back on the last 25 years.

Best decision that set me up for success:

Life: Marrying my wife.

Career: Sticking with energy and accepting Don Textor’s offer to join Goldman research when I had offers to go to other firms and cover non-energy sectors.

Worst decision I am lucky to have overcome or avoided:

Life: Just because I have never overtly looked overweight should not be confused with actually being healthy; thanks to both my long-time personal care physician and my wife for setting me on a healthier track.

Career: Nearly leaving Goldman early in my career for seemingly more dollars being offered at other Street firms.

Favorite non-Super-Spike macro call/decision:

Life: I started working from home on summer Fridays and then year-round Fridays a few years after my first child was born. This was long before it was common or even a policy. I just did it and loved doing the school drop-offs and pick-ups when my kids were in elementary and nursery school.

Career: The work we did on the refining sector, especially during the Brent-WTI spread years, was some of my favorite macro analysis aside from our Super-Spike call.

Favorite trip:

Life: It’s a close call but the summer 2012 trip to Jackson Hole when the kids were young I will call my favorite family vacation.

Career: There are way too many great analyst trips to just pick one, but my first Middle East visit in 2005 to Kuwait City, Doha, and Ras Laffan with my friend and former colleague Chukri Moubarak stands out.

Favorite child or junior analyst:

Life: My oldest is my favorite first-born kid, my son is my favorite boy, and my youngest my favorite baby. All three are absolute miracles.

Career: This is a tough one as I had A LOT of great junior analysts during my time. In this category, I am counting only the ones that directly helped me on the stocks where I was lead analyst. We had the Will and Joe team followed by Dok and Matt in the later years. Earlier in my career it was Jonathan and Sangam followed by Amil and Luis. Rakesh gave me my start. They all made a huge impact at different points in my career. For those of you wondering, I hired Neil Mehta into my business unit (and research department), but he was never my direct junior person; he worked in coal/alternative energy and then for our utilities analyst. I think I’ll have to give this recognition to the one person that was there for all 15 Goldman years but was not actually my junior analyst. Kim Young was my long-time assistant who started that same week I launched coverage. She is still at Goldman and was always there for me though all the craziness that encompassed my Goldman research career. Thank you Kim and congratulations on your 25 years at the firm!

One call I would like to do over:

Life: It has never made sense to stay at non-top-of-the-line hotels on vacation. You are still paying a lot. Basically, why stay at a run-down Hilton or Hyatt if there is a Four Seasons or better. If there is reason to save money, a new Courtyard by Marriott or equivalent is a much better option than a tired, near-luxury hotel. The barbell strategy often works with stocks; it is true with hotels.

Career: The 2012-2014 period at Goldman when I was co-Director of Research but remained lead analyst on the integrated oils & refiners was a period when my macro/sector view was weakest. There was a T. Rowe analyst at the time who reflected on our work and essentially told me that based on my framework, we were in the early days of a structural decline in Energy. He nailed it. I retired in 2014.

Best controversial call I made:

Life: Retiring from Goldman in 2014 to spend more time with my kids and wife is one of the best decisions I have ever made. If you are ever in position to do so, you should do it too.

Career: There is only reasonable answer: Our original Super-Spike call.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

In a major, first-of-its-kind milestone along ESG's relentless march to its grave, a federal court has ruled that American Airlines breached its duty to employees by tapping ESG-addled BlackRock to manage part of its 401(k) plan.

https://www.zerohedge.com/markets/judge-american-airlines-esg-tainted-401k-breaches-fiduciary-duty-workers

Hi Arjun,

Here is another column on how the overzealous of decarbonization by Gustavo Petro has led impoverish the Colombia and increase carbon footprint. I don't know if Mr. Petro has received the first tranches of cash for a $40 billion climate investment plan before Trump cuts it off. Two months ago, Colombia was hoping that Biden would speed up the process.

https://www.bloomberg.com/news/features/2025-01-13/colombia-s-lng-imports-threaten-gustavo-petro-s-climate-push