Crude Oil Commodity Markets 101

How I understand and interpret commodity market signals

I've spent the past three weeks discussing my Super Vol framework (here, here, and here). Based on some of the incoming questions, I am taking a bit of a step back this week to provide a "Commodity Markets 101" of sorts to offer my take on how I interpret various market signals and information. The nature, meaning, and insights found in commodity markets is not particularly well understood by those that don’t live and breathe it day-in, day-out. I will note that my background is as an equities research analyst, not a commodities trader. Therefore I offer my apologies in advance to actual commodities traders that read Super-Spiked and who may not fully subscribe to my characterizations.

I would also like to introduce a new twist on the Q&A styled notes: True or False. Here are the questions. Answer key is at the end (and within each section).

True or false?

The oil forward curve predicts what oil prices will be in the future.

Changes in the shape of the forward curve provides some of the best real-time insight on supply/demand (S/D) balances.

Inventory builds are always bearish for spot oil prices.

The long-end of the curve (months 36+) signifies the long-term clearing price of oil.

If you believe crude oil prices will triple over the next 3 years, you should "buy and hold" the front month NYMEX contract.

Short-term trading dynamics can impact spot prices.

If “speculators” were eliminated from oil markets, it would be less volatile and less prone to price spikes.

(1) TRUE OF FALSE? The oil forward curve predicts what oil prices will be in the future

False. The forward curve reflects supply/demand realities and expectations as of the moment you are observing it. Future prices are not a prediction of where prices will be in the future. Rather, they reflect the price you could buy or sell a future quantity of crude oil (or natural gas, etc.) today. Let me go with an example to hopefully clarify.

Let's say the spot (i.e., current) price for WTI crude oil is $110/bbl and the 12-month forward price for WTI is $90/bbl. Clearly the price of crude oil today is $110/bbl. The $90/bbl forward reflects the price a seller (or buyer) could choose to "lock-in" today for delivery (or receipt) 12 months from now. It's not a prediction of what that price will be 12 months from now.

If you are a buyer of the 12-month forward WTI oil price at $90/bbl, presumably you think it will be at least $90/bbl in 12-months. A seller would presumably think it will be no higher than $90/bbl. That's all that is happening here. I am simplifying the intentions of the buyer and seller. In no case does the futures price reflect a prediction that the price will be $90/bbl in 12 months. And it is entirely possible the buyer or seller has no view on the 12-month forward price but is instead locking in the time spread. You can certainly choose to use the futures price as a prediction—it’s just not going to do a very good job of informing where future oil prices will actually end up.

You can see this clearly in Exhibits 1 and 2 below, which looks at where spot prices traded relative to what the 12-month forward price was 12-months earlier. Clearly, the 12-month forward price is not a very good predictor of where spot prices will be in 12 months!

Exhibit 1 graphs spot WTI oil prices versus the 12-month forward WTI contract from 12-months prior. The point is to show the divergence between the 12-month forward contract and what the spot price in 12 months actually was. Exhibit 2 graphs that difference, which ranges from $60/bbl higher or lower than expected and usually +/- $20/bbl. Needless to say, the 12-month forward price does a poor job predicting the oil price in 12 months and is not what it represents, in my view.

(2) TRUE OR FALSE? Changes in the shape of the forward curve provides some of the best real-time insight on S/D balances

True. The old line courtesy of my former colleagues in Commodities Research at Goldman was "the truth is in (the shape of) the forward curve". Simplistically, if the forward curve is backwardated (spot price higher than forward price), the level of current demand is exceeding the level of current supply. If the forward curve is in contango (spot price is lower than forward price), current supply is exceeding current demand. Note the focus on “level” as opposed to growth rate. Commodity markets are physical in nature, not anticipatory.

I am again specifiying this reflects current supply/demand. If the forward curve is steepening, supply/demand is getting tighter and vice versa. I would also emphasize that backwardation or contango is a current consideration; it is not a prediction that supply/demand will tighten or loosen in the future. It is not a predictor, which is important to remember. For example, someone who is bullish crude oil might highlight current backwardation. But it is not a reason on its own to stay bullish unless you think that tightness or other considerations will support a bullish view going forward.

Exhibit 3 graphs WTI time spreads versus crude oil inventories. Investors often believe that spot oil prices correlate with inventories when in fact it is the time spread that correlates.

(3) TRUE OR FALSE? Inventory builds are always bearish for spot oil prices

False. Nothing was more frustrating for the perma-bears during the 2000s Super-Spike era (some of whom are still around for this cycle!) than the 2004-2007 period where crude oil inventories were building, front end time spreads became contangoed, but spot prices rose. How did this happen? In a nutshell through strength in the long end of the curve. I will again give my former Commodities Research colleagues credit for the tag line (paraphrasing) “concern about long-term shortages is creating near-term surpluses”, which perfectly describes the 2004-2007 contango bull market.

You can think of the spot price of crude oil as long-dated oil plus the time spread. Over 2004-2007, time spreads weakened consistent with inventory builds, but absolute spot prices were overwhelmed by the much larger rally in long-dated oil.

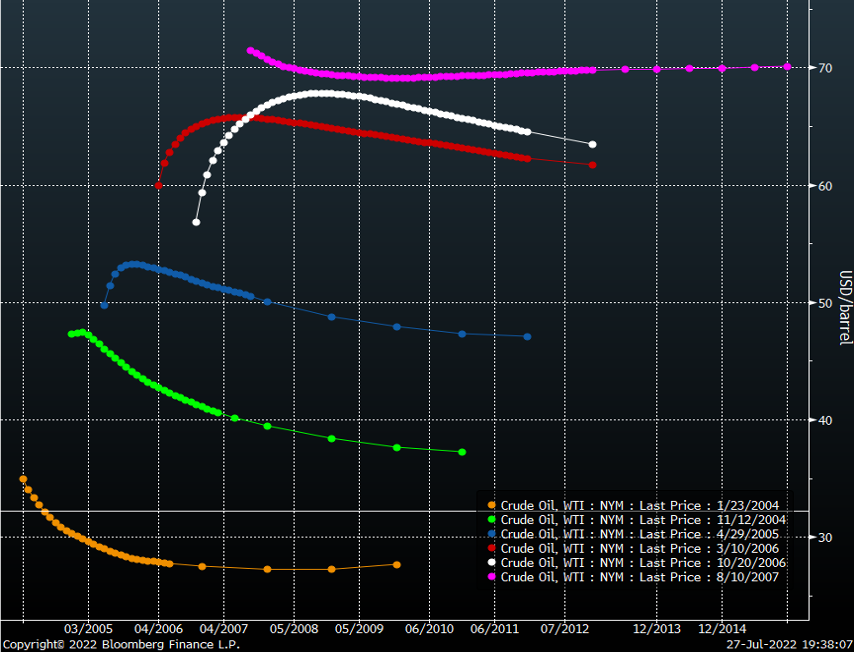

Exhibit 4 shows that crude oil inventories generally rose from November 2004 until May 2007. Exhibit 5 shows the forward curve for WTI on the dates indicated in the legend. The first forward curve data series is for January 23, 2004 where the curve is backwardated. In November 2004, the front end of the curve flipped to contango, consistent with crude oil inventories starting to build. Yet the entire curve is higher as is the spot WTI price. This pattern continues for the next 3 curves shown—April 2005, March 2006, and October 2006. Crude oil inventories are building, the contango in the curve is steepening, yet the overall price level is higher driven by a sharp rally in long-dated WTI. By the time the curve moves back into backwardation in August 2007—consistent with crude oil inventories starting to fall—the overall price level is 2X-3X where is started. It is worth spending time studying this history. It sure feels like we are on the verge of repeating this pattern in coming years.

(4) TRUE OR FALSE? The long-end of the curve (months 36+) signifies the long-term clearing price of oil

True. As should (hopefully) be clear by now, the long end of the curve reflects current expectations of where long-term prices will balance supply/demand. Clearly that view can and will change as we have seen over the past 20+ years. It’s no more a predictor than anything else discussed in this post. It’s a current representation of long-term expectations.

Exhibit 6 graphs spot WTI and long-dated (60 months forward) WTI on the left axis and (traditional) energy sector ROCE on the right axis. A few points: (1) long-dated WTI is not static; it will move with expectations of where long-term supply/demand/ROCE settle out; (2) it isn’t “right” per se; it is a moment in time representation of the long-term expectation and that expectation can change every day—faster than actual fundamentals likely change; (3) the nature of both investors and corporates is to be backward looking on the outlook for long-dated oil. I could write an entire note about this…maybe I should. The evolution of long-dated WTI oil is going to be very interesting in coming years given all the cross currents that exist.

(5) TRUE OR FALSE? If you believe crude oil prices will triple over the next 3 years, you should "buy and hold" the front month contract

False. You can argue this is either a trick question as it is not possible to “buy and hold for three years” by definition the front month contract or I haven’t adequately clarified whether I was including the ability to roll the contract when it expires. Regardless, crude oil futures contracts stipulate physical delivery to a specific location on a specific date. Unless you own physical storage infrastructure (a tank, terminal, ship, etc.), you can not "buy and hold" a particular month’s crude oil via futures contracts.

If you think oil prices are going to rally, the proxy is the upstream producers that own physical crude oil reserves. Of course, you take on additional risk via execution, cost and CAPEX, taxes, and public policy, among other issues. If you choose to roll the contracts forward, you take on the risk of changes to the shape of the forward and how that (potentially meaningfully) impacts tracking error relative to simply looking at price moves in the continuous front month contract.

(6) TRUE OR FALSE? Short-term trading dynamics can impact spot prices unrelated to S/D fundamentals

True. Successful traded markets are dependent on both fundamental players and speculators. When you have speculators in a market, you will have price moves that at times are divorced from fundamentals. So what. The liquidity and price discovery provided is ultimately critical to a healthy, functioning market. The definition of “excessive speculation” is as follows: price moves that politicians don’t like. While dynamics around leverage and use of options is deserving of evaluation from regulators, the phrase “excessive speculation” should be eliminated from the English language.

(7) TRUE OR FALSE? If “speculators” were eliminated from oil markets, it would be less volatile and less prone to price spikes

False. Read about the 150 year history of the oil business, most of which did not include an active futures market. You can start with Bob McNally’s great book Crude Volatility (Amazon).

Exhibit 7 graphs oil market volatilty since 1865 which I have defined as the one standard deviation move in annual oil prices over a 5-year period divided by the corresponding 5-year average. The underlying oil price data comes from BP’s excellent Statistical Review of World Energy annual publication (BP uses a range of historical indicators to represent “oil prices”). You can observe the structural decline in volatility from 1865-1970 as a combination of the Standard Oil Trust, the Seven Sisters and the Texas Railroad Commission sought to temper inherent volatility, with some success. NYMEX trading only began in the 1980s, with volatilty in a remarkably stable band since then. The point here is that NYMEX (or ICE or any other exchange) is NOT the reason oil markets are volatile. Rather volatilty stems from a combination of the inelasticity of supply, inelasticity of demand, the physical and complex nature of oil markets, and geopolitical turmoil. It is inherent to the business.

Answer Key

(1) False (2) True (3) False (4) True (5) False (6) True (7) False

Scoring results:

7 correct: Congratulations! You must be a professional crude oil trader!

6 correct: Congratulations! You must be one of the better energy equity research analysts or energy dedicated investor!

5 correct: You have friends that trade commodities or are energy equity research analysts and have been long energy since near the pandemic trough.

4 correct: You win your share of coin flips.

3 correct: You lose your share of coin flips.

2 correct: You are a FAANG investor chasing energy performance.

1 correct: You are an unprofitable tech investor chasing energy performance.

0 correct: You are a member of Congress…perhaps on track to be President!…or at least White House press secretary.

⚡️On a personal note…

TRUE OR FALSE? I should have switched to the tech sector in the late 1990s when I had the chance.

You know the answer: FALSE!!! I had a few (decent) opportunities to move on from energy at a time I had seven years experience in the sector, three at Petrie plus four at JPMIM. But I enjoyed the global nature of oil & gas. It was clearly a critically important sector even during the out-of-favor decade of the 1990s (in 1999, I had no inkling another super-cycle was even remotely possible). And I enjoyed interacting with the sector management teams and employees. Oil & gas has always attracted contrarian types; when it's in favor, everything else is out of favor and vice versa. As I noted in an early Super-Spiked post, it's a classic bizzarro world sector.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Regards,

Arjun

📘 Appendix: Definitions, Clarifications and Sources

Backwardation. Spot price is higher than forward price. Occurs when the level of demand is higher than the level of supply.

Contango. Spot price is lower than forward price. Occurs when the level of demand is below the level of supply.

Spot oil price. The price of oil today.

Forward oil price. Today’s expectation of the price of oil in the future.

Strip oil price. The average of the spot and forward prices of oil over a particular period of time. For example, the 12-month strip price would average the price of the monthly oil contracts for the next 12 months (month 1 is spot).

Forward oil curve. Similar to the strip, but usually used when discussing the visual manifestation of the forward price curve structure.

Time spread. The difference in oil price measured by oil forward contracts for different months. For example, the 1-2 time spread measures the difference between the spot contract (month 1) and the next month’s contract (month 2). A positive number would indicate backwardation (month 1 is higher than month 2). A negative number would indicate contango (month 1 is lower than month 2).

CL1. The Bloomberg ticker symbol for spot WTI crude oil.

CL12. The Bloomberg ticker symbol for the 12-months forward WTI crude oil contract.

C01. The Bloomberg ticker symbol for spot Brent crude oil.

Per your endorsement I bot McNally’s “Crude Oil Volatility” 🙂

Great article...so many basic misconceptions.