Earning The Right To Grow

Corporate Strategy

The macro backdrop is shifting from an obsessive focus on “energy transition” and the negative framing of energy usage that accompanies “the urgent climate crisis is all that matters” worldview to one where meeting growth in global energy demand is regaining its rightful prominence. As a reminder, growth in energy usage means the world is becoming richer; it is one and the same with economic growth and higher employment; it is people being lifted out of poverty; it is lower- and middle-income people seeing improving lifestyles; it is the rich world enjoying their existing wealth. It is consistent with cleaner air and cleaner water, though not always with protecting biodiversity. Geopolitical imperatives in major developing world countries will drive long-term progress on new energy sources and technologies that by definition will be lower carbon in nature.

The narrative shift has been a long time coming, given the significant unmet energy needs of the other 7 (soon to be 9) billion people on Earth that are not amongst The Lucky 1 Billion of Us. But in the near-term it is Big Tech and the emergence of artificial intelligence-driven power demand that is reminding everyone that the reason we use energy in the first place is to “better human lives” (here). It is a welcomed shift.

2024 is on-track to be the fourth year of better profitability for the traditional energy sector and in particular companies in the top two profitability quartiles. With structurally improved returns on capital becoming a fact and not simply a forecast, the next stage of recovery for traditional energy we think requires a return to some form of growth—organic, inorganic (i.e., M&A), or much more meaningful share buybacks to generate leading per share growth metrics. Returns AND growth is what defines stock market leaders. Given the inherent maturity of traditional energy, long-term stock buybacks coupled with M&A is likely to be a winning combination, as we highlighted last week via the Murphy USA example (here). The trick with M&A is to not ruin returns by overpaying for the wrong assets or wrecking the balance sheet at the wrong time in the cycle. The trick with stock buybacks is to avoid being pro-cyclical when executing.

The foundation of “earning the right to grow” includes:

Best-in-class execution on existing asset base

Mid-teens-plus CROCI and ROCE at normal/above-normal portions of the cycle, cost-of-capital profitability at a normal trough, and break-even at a deep trough

Free cash generation at mid-cycle or better pricing and around break-even at trough

Fortress balance sheet including an accumulation of net cash at the higher points of the cycle

Options to grow include:

Long-term, consistent share buybacks for companies devoid of meaningful organic growth options

Inorganic via merger and acquisition (M&A) activity

Organic via exploration (upstream) or new project expansions (upstream, midstream, downstream)

The de-growth assault on traditional energy is coming to an end

Traditional energy companies have been at the epicenter of “the world has to transition right now due to the urgent climate crisis” spell the world has been under, which started toward the end of what was a challenging post-super-cycle extended bust period during the 2010s. Weak profitability and share price performance drove investors to demand companies go ex-growth and prioritize improving profitability.

There was frankly little daylight between climate activists demanding an end to fossil fuel investment and most traditional investors demanding an end to production growth as the defining corporate objective for upstream-oriented companies in particular. The modern ESG (environmental, social, and governance) movement has been the bridge between climate activists and traditional investors looking to elevate various environmental and social objectives to be on par with the core mission of a publicly-traded company, which is to generate profits for its investors.

In recent years, ESG has morphed from being a behind-the-scenes evaluation of relevant non-financial risk factors to one that was consumed by the western world’s climate and social justice movement. We believe ESG should revert to its historic below-the-radar positioning with as much emphasis on areas like governance and non-climate environmental considerations and not merely de facto “urgent climate crisis” advocacy.

What does it mean to “earn the right to grow”?

The purpose of publicly-traded companies is to profitably produce goods and services society demands. The operative words are “profitable” and “demand.” Profitability was a problem for much of the traditional energy sector last decade (US downstream companies were a notable exception) and there is an ongoing debate on how much longer oil and natural gas demand will continue to grow.

2024 looks to be the fourth year of much improved profitability for the sector and we believe essentially all companies have taken to heart the need to focus on corporate-level return metrics like CROCI (cash return on gross capital invested), ROCE (return on capital employed), and free cash flow. On the demand front, we have written extensively about our view that there is not a decade let alone year when anyone can possibly know when oil or natural gas demand will permanently peak or plateau. The unmet energy needs of the developing world coupled with AI (artificial intelligence)-driven power demand growth points to meaningful energy demand needs for the foreseeable future measured in many, many decades ahead. With improved corporate-level profitability now a core focus of every company and energy demand clearly on track for meaningful growth in coming decades, there is an opportunity and imperative for companies to help meet the world’s energy needs.

So every company now needs a growth strategy?

That is not our view nor what we are saying. There are indeed companies with mature asset bases and limited reinvestment opportunities that are best suited for a long-term liquidation strategy (massive cash returned to shareholders or sale of company).

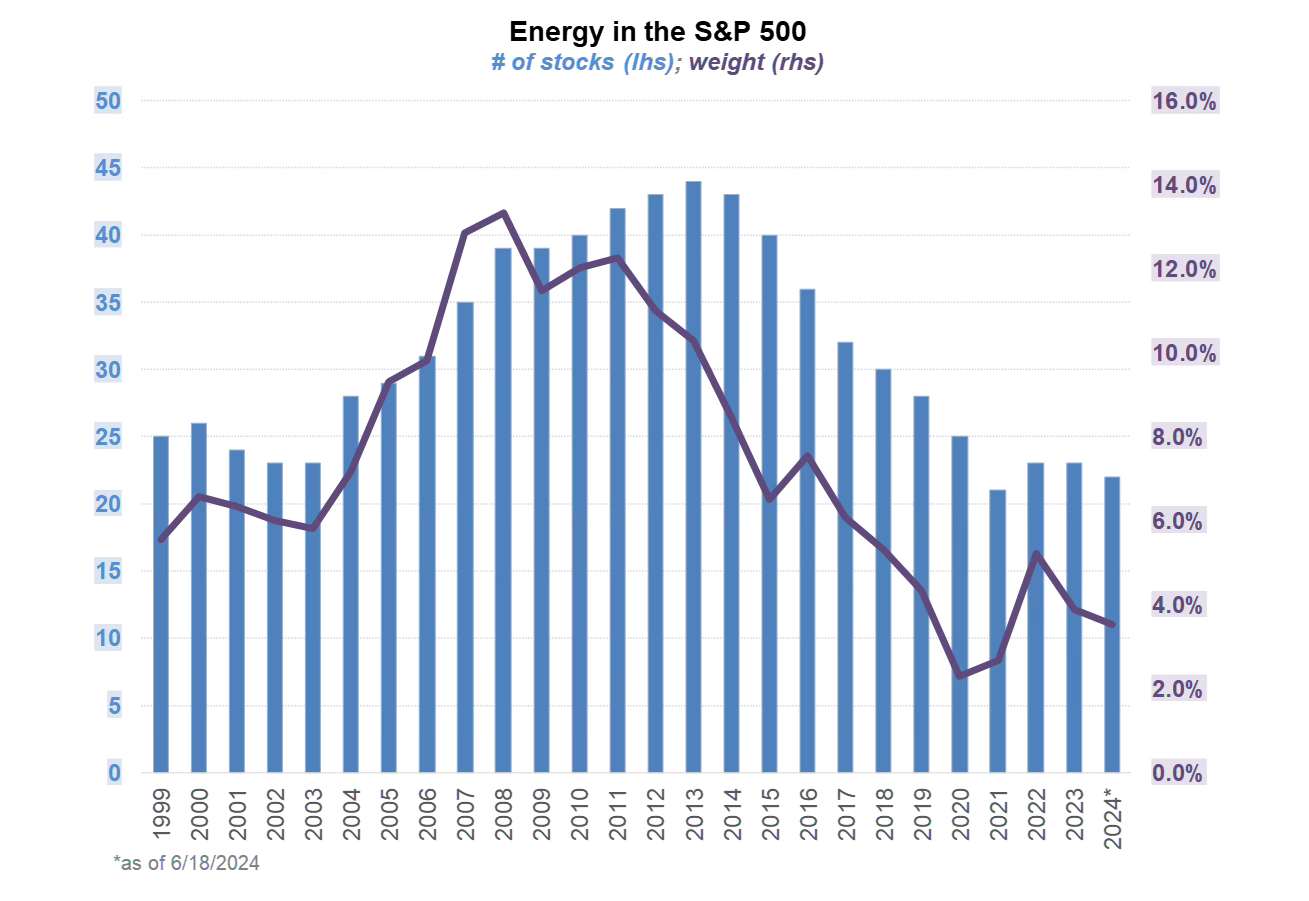

For everyone else, the ability to explore, develop, transport, process, refine, market, and trade oil and gas is a critical skillset contained within a shrinking universe of companies (Exhibit 1). There are only so many geoscientists and engineers on Earth that would rather work in oil and gas versus a hot technology company. Very few people or companies have the ability to run an oil refinery or natural gas processing plant. Oil and gas pipelines are probably already rarer than fiber optic data lines. How many companies are there that can efficiently run LNG trains? Not many.

Exhibit 1: A shrinking universe of investable energy companies in the S&P 500

Source: Bloomberg, Veriten.

The most pressing energy needs right now are in the power sector, which has not historically been part of the opportunity set for most oil and gas firms (upstream, midstream, downstream, or integrated). In contrast to our long-standing view that most traditional energy companies should NOT pursue aggressive new energies strategies, we are open-minded to an evaluation of power sector opportunities.

As we noted in last week’s video podcast (here), a combination of inorganic growth (M&A) plus long-term stock buybacks may be the answer for many traditional energy companies (Exhibit 2). Some will naturally be sellers; others consolidators. There is no one size fits all strategy or solution. Our point is simply that the investor (and activist) demand that the entire sector remain ex-growth does not match the profitability and demand profile we see.

Exhibit 2: Massive stock buybacks, excellent execution, and M&A has led to significant stock price appreciation for MUSA shares

Source: FactSet, Veriten.

Why has grow(th) been a four-letter word in energy?

Prior to the devastating COVID trough, far too many traditional energy companies paid far too little attention to corporate level profitability metrics. The story is now well known so we will be brief. The excessive focus on well (or project) level internal rates of return (IRRs) led companies to falsely believe they were making wise capital allocation decisions, which often was not the case. We believe that problem is now in the past. We see this mistake being made in the renewables space via the flawed levelized cost of energy (LCOE) metric that is very similar in spirit to well IRRs.

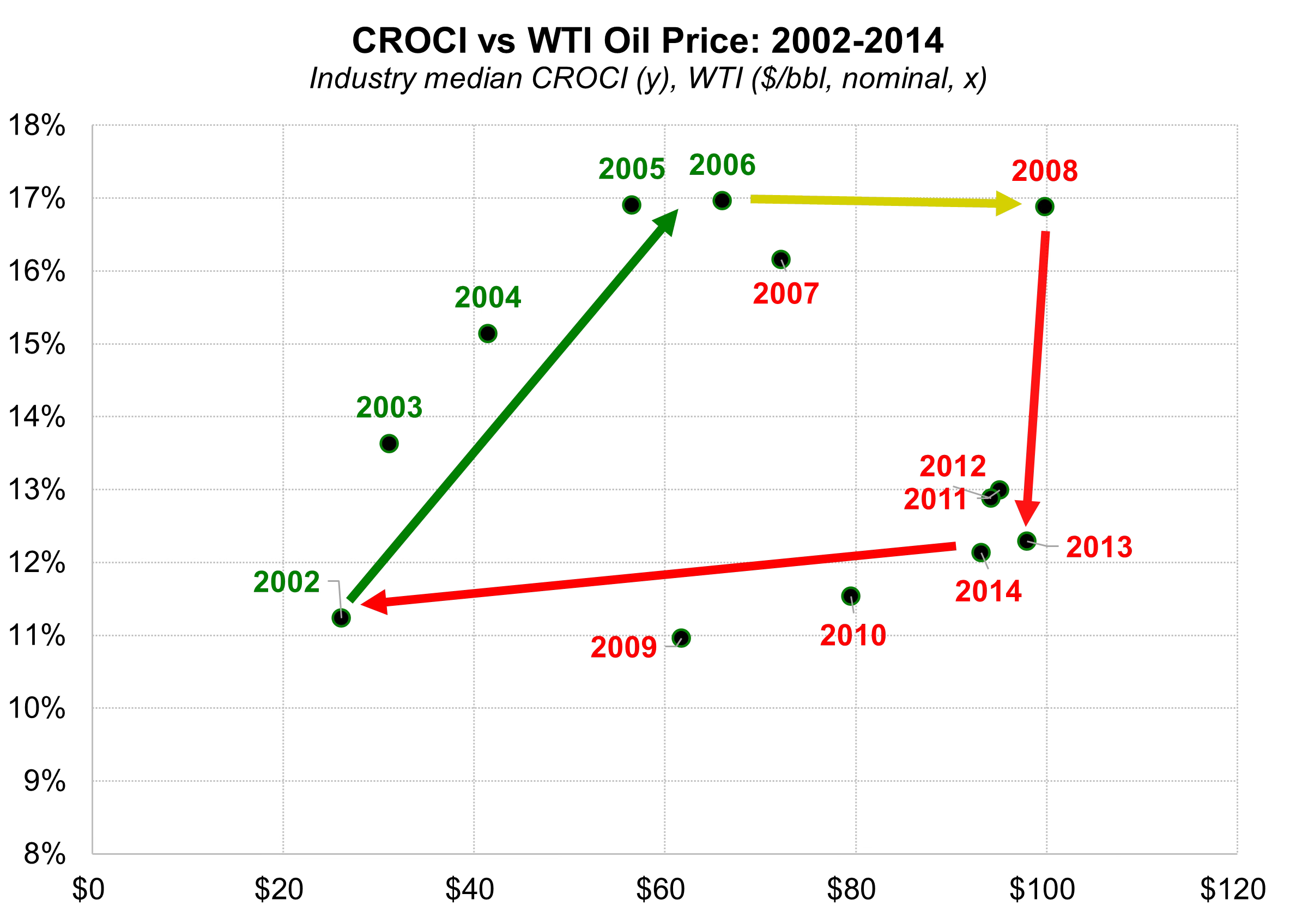

During the 2004-2014 Super-Spike (super-cycle) era, capital spending rose substantially as oil prices structurally increased. Ultimately, a mixture of cost over-runs, timing delays, and eventually falling commodity prices led to a collapse in profitability that we have branded “The Quadrilateral of Death” (Exhibit 3). We will never forget that disaster.

Exhibit 3: Never forget the Quadrilateral of Death, where excessive capital spending led to a collapse in profitability despite a 4X-5X jump in oil prices

Source: Bloomberg, FactSet, Veriten.

Won’t greenlighting growth raise the risk of return erosion?

Demand for all forms of energy is growing. Solar is growing at a fast rate. Electric vehicles are growing at a decent clip, even if the pace has slowed in some regions. Crude oil and refined products are growing at a modest rate, but well ahead of “peak demand” concerns. Natural gas growth is likely to accelerate due to the bullish inflection in power demand. We need energy companies to supply all the forms of energy that are in demand. In our view, the world is a better place when US, Canadian, and European traditional energy companies are healthy and part of the solution.

No one can guarantee that capital allocation mistakes won’t be made. That comes with risk taking. But there is no ability to return excess cash to investors without investment in the first place. Dividends and stock buybacks do not fall magically from the sky. They are an outcome of advantaged investment decision making.

What are good growth metrics?

Growth in returns (CROCI, ROCE), earnings and cash flow per share, life-of-asset/project/company free cash flow per share, and balance sheet cash.

What are bad growth metrics?

Absolute or per share production volumes. We would encourage companies to steer clear of emphasizing production growth like they did in the past. The focus should be on earnings, cash flow, free cash flow, profitability, and balance sheet metrics and how those figures will improve based on an investment strategy. Is your 3-, 5-, or 10-year plan better or worse relative to an ex-growth strategy? What are the risks? How is it stress tested for the inevitable normal and deep trough that will occur in a cyclical commodity business? What are the main execution risks relative to an ex-growth model? How is progress tracking along the way versus what was promised?

Why give companies a get-of-jail-free card to ruin profitability?

No one is doing any such thing. Much like we push back on the “you must urgently transition now” narratives, it is apparent that an ex-growth mentality will not lead to broad-based outperformance of the energy sector even as it might be correct for some individual companies. Leading S&P 500 companies offer an attractive combination of returns AND growth that traditional energy will need to compete with if it is to attract incremental investor dollars. That said, the inherent maturity of the sector supports a greater emphasis on M&A plus long-term stock buybacks rather than organic growth.

Is near-term profitability dilution acceptable if taking on new projects or M&A?

It depends and is really a case-by-case question. There are times when near-term dilution to CROCI or ROCE is acceptable, but with increased execution risk that the asset (or company) being bought will have a sufficiently sizable and low cost of supply opportunity over the long run to more than offset the near term dilution. If there is a risk of giving companies a “free pass” on ill-advised spending, it is here.

We believe there is a need for companies to return to long lead-time projects in areas like LNG (liquefied natural gas), deepwater exploration, and other long-lived projects (e.g., heavy oil, oil sands, and other non-US shale, conventional developments). The nature of upfront spending necessitates near-term returns dilution. Similar to M&A, evaluation of risks should be done on a case-by-case or company-by-company basis.

What are the signs of undisciplined growth?

Deterioration in profitability at a given oil price, recognizing there does need to be a tolerance band for upfront spending. As an example, long lead time projects that require several years of upfront spending prior to start-up will negatively impact short-term profitability. There is no hard figure that up to a 2% near-term dilutive impact to returns is tolerable but any more is not; it really depends on the company and risk/reward of the project or asset. Balance sheet metrics and stress testing exposure to inevitable downcycles help determine how much growth exposure is too much.

Isn’t it foolish to be talking about growth when concerns about recession and economic slowdown still exist?

Quite the contrary. There is no better time to be contemplating what could make sense from a long-term growth perspective if we are in fact headed into a period of economic and commodity price weakness (not our base case, but ALWAYS a risk). Nothing we have written argues for aggressive capital spending to lift a near-term production growth rate over the next 12 months. Companies ought to be thinking about what types of assets or projects could be worth legging into if oil prices were to break to the downside over the next year. Perhaps that would be the time to consider a more meaningful stock buyback program or to engage in counter-cyclical M&A.

⚡️On A Personal Note: Answering OAPN reader questions

What did your wife and kids think about your empty nest commentary in last week’s video?

As predicted, there is zero evidence any of them watched it, so no feedback was received or is expected. That is 100% their loss on missing out on exciting MUSA stock buyback perspectives. There is more to life than the Mag 7 family! Maynard watched it and sent a nice note which was both thoughtful and appreciated.

You seem to talk less about your golf game than in the early years of Super-Spiked, how’s it going?

I’ll have to double check but I don’t feel like my golf commentary is any less frequent. I have been able to broadly maintain the high single digit GHIN that I reached pre-Veriten. It’s not too hard to get rounds in, but practice time remains way down. As I noted earlier this year, I am committed to getting in more practice time this spring and summer. We have a great short game area at our club and that remains the focus.

What are your vacation plans for the summer?

A downside of no longer having captive kids is that planning family vacations is now subject to their work and internship schedules. To the credit of my children, none want to work remotely and have prioritized in office experiences. So it looks like we are doing a bunch of mini-trips and not always with the full five person complement. I am looking forward to Colorado and Scotland visits and will also get to Cape Cod where my parents live.

You seem to travel a lot more with Veriten, how’s that going?

So far, so good! In comparison to my 15 years at Goldman Sachs, everything else feels like part time work. Veriten travel is almost entirely for what were the favorite parts of my old analyst job: speaking with boards/management teams or at various conferences or industry events. That is a cake walk compared to breakfast-through-dinner, hourly investor meeting schedules before flying coach to the next city. The old nine European cities in five days slog will never be repeated.

Now that you are an empty nester, what about moving to Houston, which would cut down on travel?

Houston has really grown on me over my 32 year career. It has a vibrancy today that I don’t remember from earlier in my career. My wife needs to visit and have a good time on that trip(s). I wouldn’t expect to become a permanent resident, but a condo could be in our future. February-April and September-October tend to be heavy travel periods to Texas so might as well stay during those months. We just need to work out the logistics to enable our golden doodle to fly with us…which won’t be on United. Yankees-Astros at Minute Maid and Knicks-Rockets at Toyota Center will be fun to catch in person. America’s Team is a short flight away. I am OK subscribing to MSG+ for Rangers hockey. I have no idea what conference realignment will mean for the ability to watch USC or the University of Colorado versus local Texas schools.

You are still on a bunch of boards and advisory boards, how does that work with Veriten?

I find great synergy between my various board, advisory board, and senior advisor roles and Veriten. All are energy focused but with different vantage points on the sector. It is clear to me and I would hope to everyone I come across that the broader perspectives gained help inform my overall view point as ultimately reflected in Super-Spiked and Veriten meetings. Navigating potential conflicts of interest was part of being a Goldman analyst. One needs to recuse oneself in some situations, to not be “wall crossed” in some instances, and to be transparent when appropriate about where and how you are engaged.

As many of you will appreciate, it is the local charity boards that are the time and energy sinks. I believe there is a need to give back, but it sure tests one’s patience.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Arjun:

I have been a reader and follower for a while and find the articles and perspectives insightful, helpful, always backed by thoughtful research and observations. Hence the recognition of MUSA strategy and execution were particularly gratifying.

This weeks article is on point and timely as well as we struggle in the E&P sector to balance growth, capex and hopefully expansion of cash on cash returns with fact one gets hammered for capex growth. My belief, unsurprisingly, is that a huge component of balance sheet management should include long term, consistent share repurchase. This is harder in the upstream sector as it must be underpinned by solid earnings.

In any event, I enjoy the articles and took the opportunity to share last weeks MUSA shout out with my management and board.

Madison Murphy

Always insightful Arjun, thanks!