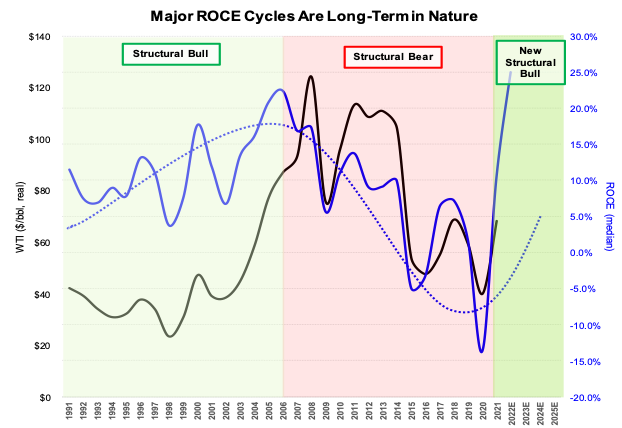

Evolution of a Structural Bull Market: The PTSD Pullback

Where Are We In The Energy Cycle

COLLAPSING US nat gas and lackluster crude oil.

CAPEX inflation.

RETURN of mega projects.

DOWNWARD Street EPS revisions.

DIVIDEND (variable only) reductions.

We've been here before! Whether you are a veteran investor of past super-cycles or a newbie that only knows the post-Great Financial Crisis energy sector hellscape, the PTSD is real.

In my ROCE Deep Dive series and related posts (scroll down here for links to ROCE Deep Dive posts on right side of Super-Spiked website), I have spent considerable time focused on the long-term profitability cycle for traditional energy, which I have characterized as 10-15 years of good times followed by 10-15 years of underperformance. Coming off the 2006-2020 ROCE downcycle, I have been of the view that we are now in year 3 of what I would expect to be a new 10-15 year period of better profitability for the sector. There is no change to that view.

What I have not done heretofore is to comment on the evolution of how the structural up (or down) cycles progress, which I will start to do with this post. As I have said many times, Super-Spiked is not an investment newsletter so none of this is meant to infer a trading call for traditional energy equities. There is plenty of interesting Street research covering the short-term outlook and the timing of this commodity or that stock rebounding or collapsing further. I'll leave that to the pros. As always, Super-Spiked will try to look through the noise and take a longer-term approach to shorter-term issues.

I think we can conclude that Phase 1 of the messy energy transition era is over. Some call it the "easy money" phase, but investing at the trough is never easy and those that have the guts and timing to do so are deserving of praise. We have moved into Phase 2 and await Phase 3. Choppiness is increasing and with it, as always, comes opportunity.

Evolution of a structural bull market

This post is overdue and, frankly, if I was still co-Director of Americas Equity Research of a major Wall Street bank, I would gently (or perhaps not so gently) let my analyst know that it is late. My thought was I would avoid the short-term stuff that the Street typically focuses on. But I think I had too much of a Street analyst view of what it means to discuss the short-term. It can still be framed from a strategic perspective and there are plenty of opportunities for investors and strategy decisions for executives that come out of the short-term noise that is absolutely worth discussing.

So here is a short summary of how I see the main phases of a structural bull market:

Phase 1: Rally Off Trough

Costs are low.

CAPEX is low.

Beginning valuations assume trough conditions continue into perpetuity.

Commodities surprise to the upside.

Deep value investors dominate and demand discipline, debt paydown, max dividends/stock buybacks, and no growth operating philosophies.

This is the October 2020 - June 2022 period.

Phase 2: The Transition

The capital spending cycle begins.

Inflation returns, costs rise.

Inevitable commodity volatility creates cycle duration uncertainty.

Deep value investors are selling the sector; mainstream funds are nibbling but are not fully back-in.

This is what we have been experiencing since mid-2022: "See, I knew I couldn't trust this sector to generate sustainable outperformance. Back to growth tech!"

Phase 3: The Long And Winding Upcycle

It turns out it wasn't "over" for the commodity cycle.

Differentiation between good and bad companies becomes more noticeable, even if at times ignored.

Who is spending capital wisely?

Which projects or acquisitions make sense?

Who is over-spending, expanding beyond core capabilities, or otherwise losing discipline?

Whose inventory is running thin?

Who is sensibly adding duration to asset longevity?

Who is being overly cautious and missing opportunities to add duration with favorable convexity?

Returns on capital overall remain at healthy levels.

Capital flows back into the sector to fund growth and acquisitions.

The sector's weighting in the S&P 500 makes a big move up.

Mainstream funds and GARP investors return to the sector.

There will be plenty of mini-cycles along the way.

Phase 4: The Peak

Commodity prices may still be rising, but ROCE is starting to seriously erode relative to commodity prices.

Drill-baby-drill is the rallying cry.

Sector valuations inflate as above-normal conditions are normalized.

Energy is in vogue: Tech sector royalty (i.e., PMs) sit in on energy sector analyst and company meetings.

Energy as a viable investment sector is dead man walking.

Phase 5: Decay, Death, and a New Structural Downcycle

We all lived through this over 2010-2020.

I don't believe further explanation is neeeded.

Navigating the long part of the upcycle with a Super Vol mindset

A reminder that there is nothing about the Super Vol macro backdrop that I think has changed:

Spare capacity is non-existent.

CAPEX remains woefully short of what will be needed to meet expected long-term oil and natural gas demand growth.

The expectation that oil and natural gas demand will peak and then decline within the next several years is way off base, in my view. For that matter, coal may yet continue to grow.

However, without a major CAPEX cycle, commodity prices are expected to regularly spike (every few years or so) in order to limit demand to available supply.

The downside of the spike period does create short-term, bearish volatility as we are currently seeing.

A Super Vol macro backdrop offers some pros and cons versus the 2002-2014 Super-Spike era:

High volatility likely results in a slower rebound in CAPEX.

High volatility likely keeps sector valuations lower than otherwise might be the case as investors perpetually fear short-term pullbacks, reinforcing an environment of capital discipline and increasing the odds of price spikes (and subsequent collapse).

High volatility means we will likely have many "mini-cycles" within the broader, structural upcycle...i.e., PTSD pullbacks regularly occur.

Management teams that are not cognizant of volatility run the risk of making unexpectedly high cost acquisitions, and, in some cases, potentially selling assets (or the company) at sub-optimal points in the cycle.

This part of the discussion has been enhanced by conversations with a new friend of Super-Spiked, a person I did not know from my analyst career that has particularly interesting takes on explicitly pricing volatility into asset and company valuation.

The new CAPEX cycle is likely what is causing the most concern among investors

While investors always worry about short-term commodity volatility, I will guess that it is the increase in CAPEX that is likely what is of greater concern at the present.

Grounding principles of spending on CAPEX, mega projects, or acquisitions:

Management team has a track record of generating competitive returns on capital.

Management team has demonstrated expertise in area of spending.

If a new area, new executives are brought on board that know the new area or project type.

A company has a clear path back to fortress balance sheet status, which increasingly may be defined as net debt free.

At the inevitable next downturn or commodity trough, a company earns a cost-of-capital ROCE at a normal trough or is no worse than break-even on earnings if it is a deeper trough.

Spending does not place base dividends at risk in the event a 2-3 standard deviation downturn in commodity prices materializes.

If investing in mega projects, a similar philosophy of these various points hold, especially when looking at the maximum point of cumulative, pre-start-up CAPEX.

So what are the signposts of bad spending?

After a rally in commodity prices, management teams emphasize strip pricing when announcing acquisitions or major projects, without providing other metrics such as trough of cycle or non-strip planning scenarios.

Companies enter new areas with an executive team that does not have expertise in that new area.

EPS (earnings per share) or CFPS (cashflow per share) accretion/dilution metrics are emphasized using strip prices (after a rally). Spoiler: when debt costs are low, it is the rare deal that is not accretive to EPS or CFPS. It’s an idiotic metric for commodity producers.

What are NOT signposts of bad spending?

Higher CAPEX in and of itself.

Higher CAPEX driven by sector-wide inflation at the start of a new upcycle, so long as spending still generates competitive returns at lower points of the cycle.

Spending on acquisitions or mega projects, so long as it similarly generates competitive returns at lower points of the cycle.

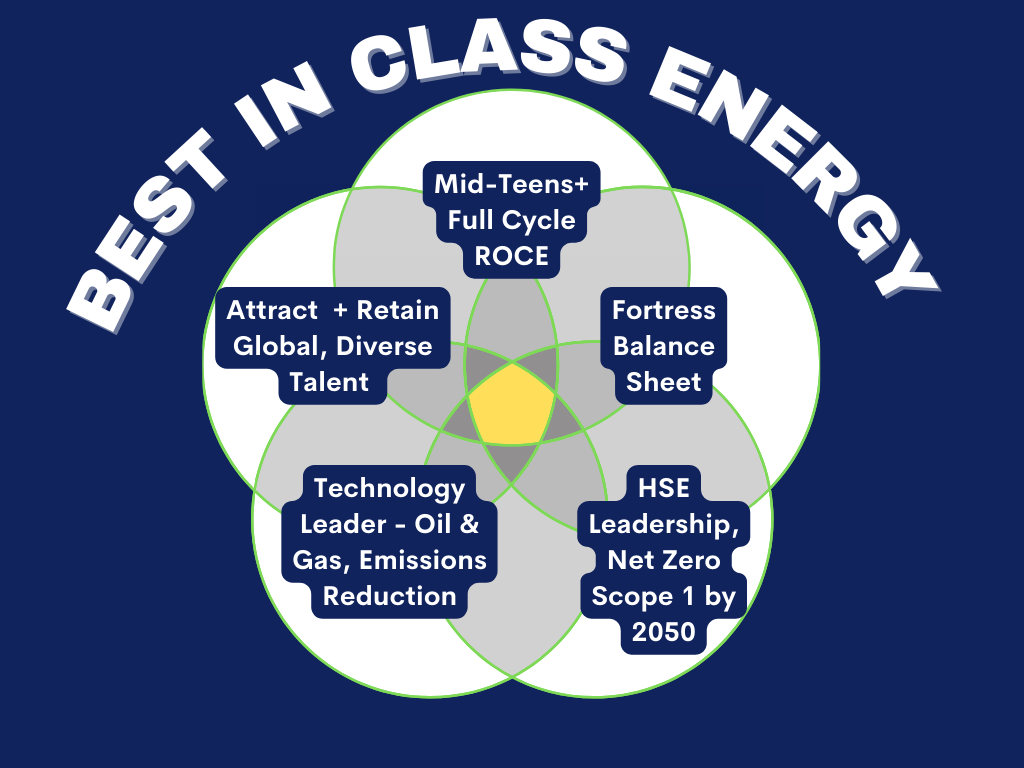

What “good” looks like for traditional energy companies

Mid-teens or better full-cycle ROCE

Trough of cycle ROCE of 0%-8% (depending on severity of downturn)

Fortress balance sheet (net debt of around zero)

Investing in projects at the low end of the future cost curve

Positioned to capture upside commodity price optionality

Diversified (for larger companies)

Cognizant of the need to eventually diversify or sell if a smaller, pure-play

Steady base dividend growth

Traditional HSE leader

Credible plan to eliminate Scope 1 emissions in coming decades

Technology leader

Ability to attract and retain globally diverse talent

What areas look interesting and under-appreciated

A partial list of areas I find interesting (feedback welcomed):

Long-cycle oil in geopolitically friendly countries: e.g., Canada's oil sands region

Middle East mega projects (fiscal term dependent): Oil and natural gas/LNG

Natural gas/LNG trading

Low decline PDP oil reserves in the U.S.

Methane abatement technology providers and service companies

Non-OECD domestic coal (thermal and metallurgical)

Cobalt resource not located in the Democratic Republic of Congo (more on this once I finish reading Cobalt Red by Siddharth Kara)

Industrial technologies (hardware and software) aimed at improving energy efficiency

Nuclear value chain

Geothermal and heat pumps

Powering Africa

ICE vehicle growth in the developing world

Areas that look overhyped:

The Hydrogen Economy: the colors are dumb…this will have a chance once the world shifts to looking at characteristics not colors.

Renewables without storage and other needed infrastructure costs included. Is there a reason LCOE doesn’t include all the costs? Feels a lot like the shale “Well IRR” debacle, but with much worse societal implications.

EVs. Note: I expect EV sales to achieve meaningful growth in coming years, just not the hockey stick upsides that seem embedded in consensus.

"Energy transition" spending for traditional energy companies

This will be the topic of a stand alone follow-up post. I recognize "energy transition" is an inaccurate term for what is occurring, but I think it is still the dominant phrasing most observers are using. I am due for a followup “Sticks and Stones” post (here).

It remains my view that the overwhelming best thing traditional energy companies—upstream, midstream, downstream, and oil services—can do is to ensure the world has abundant deliverable oil, gas, and refined products to meet the world's demand for those products.

The purpose of oil and gas companies is to profitably produce (or support the production of) oil and gas. Full stop.

As far as so-called "energy transition" spending goes, companies should invest where and when they have competitive advantage. It is possible that some newer energy technologies can make sense for oil & gas companies to pursue. An example might be the renewables fuels investments made by various refiners.

It is also clear that society is moving toward requiring all companies in all sectors to reach "net zero" Scope 1 emissions. In pursuing that goal, it is possible investment in new technologies may make sense. However, the idea that traditional energy companies MUST transition to companies focused on future technologies is an absurdity that I suspect is already in the process of passing (see recent change in tone by certain Euro Majors). The most obvious area where oil and gas companies can help mute excess greenhouse gas emissions is in the area of methane containment.

With all that said, there are some new areas that may exhibit rapid growth and where favorable tax/policy incentives exist. If an executive team can demonstrate this is a logical adjacency or that they have added unique expertise to pursue such opportunities, I personally take no issues with such spending. I might even call it modern day exploration. You can explore for crude oil, natural gas, or new energy technologies. Just don't forget what the typical probability of success is with exploration.

🎤 Streams of the Week

Volts: What's the deal with electrolyzers?: click below

COBT: “This Is An All Hands On Deck Situation” Featuring John Dowd, GoGreen Investments: link

Wicked Energy with JG: WE032 – Geothermal and Subsurface Energy Storage with Joe Batir, Geothermal Lead at Petrolern: link

⚡️On a Personal Note

The quest for new or diversifying energy sources typically occurs during periods of high and rising prices. The 2002-2012 period was no exception. I recall visiting the new energy companies of that era which included corn ethanol biofuels, soybean-based biodiesel, cellulosic ethanol, algae to biofuels, woodchip cokers, and many others.

Cellulosic ethanol was five years away from commercialization in 2005. And since I don't think anyone spends any time on it any more (do they?), it must still be at least 5 years, or perhaps 25 years, away. Corn ethanol always seemed like an ag policy, rather than an energy or environmental endeavor. Maybe if presidential primaries no longer start in Iowa, we can stop mandating corn ethanol usage (for the non-Biden fans out there, I think the president deserves some credit on this one).

One of my most memorable visits was to a company somewhere in Florida that was going to turn algae into a transportation fuel alternative. I still remember they had a conveyor belt where a worker was using the same type of plastic bucket that my kids were then using to build sand castles at the beach to catch algae coming off the conveyor belt. It looked ridiculous. I specifically remember that moment and thinking that there was no way any amount of scaling up of this project was ever going to be a serious challenge to the oil and gas industry. I am 99% sure no IPO ever materialized for that company. Thank goodness.

Will the current crop of "hope and dreams" technologies turn out better? Yes, I think some will. But do yourself a favor and visit these projects in person. And as a general rule, avoid companies utilizing children's toys in their operations.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

This part of the discussion has been enhanced by conversations with a new friend of Super-Spiked, a person I did not know from my analyst career that has particularly interesting takes on explicitly pricing volatility into asset and company valuation.

Can we read their stuff somewhere? :-)

Arjun, are you going to drop some suggestions on which of the oil and gas majors fall into the “well managed and capitalized” bucket today?

As a side comment on the projected hockey stick take-off for BEVs, I can’t see this happening any time soon. Not just on the supply side of batteries and improvement in battery tech, but due to the practical limitations of sufficient charging stations for those not so fortunate to have ample electrical supply in their garage. Looking around urban areas, there are practical limitations to building and wiring a sufficient number of high-amperage charging stations, especially for legacy multi-tenant buildings.

And any rapid spike in electrical power demand for BEV will come as many municipalities have the stated goal of shutting down fossil fuel powered electrical generation, and nuclear power plants, with no clear understanding of how deficient wind turbines and solar power are without sufficient baseload power and energy storage.

One other point often overlooked when comparing the cost of BEVs to ICE autos is the massive revenues generated by motor fuel taxes, both locally and nationally. A recent study estimated revenues of $1.20 per gallon of gas sold at the pump in California. This is revenue that the taxing authorities will not give up without a fight, meaning that if BEV sales were to dramatically increase there would be a political backlash with the electric “free rider” problem. This will lead to an increase in energy taxes or other fee structures to recoup the lost motor fuel tax revenues.