Five Big Questions for Traditional Energy at the Mid-Point of 2023

Navigating the Energy Crisis Era

Welcome to the 2H of 2023! It's always hard to believe how quickly time flies. As we did at the start of the year, we will look to address the five big questions we see facing the traditional energy sector. Year three of the messy energy transition has so far proven to have been a "pause" year so to speak, with softer global crude oil and natural gas balances in the aftermath of the sharp spike in 2022. The pullback is consistent with our Super Vol macro framework that calls for an ongoing series of spikes followed by pullbacks—Super Vol, not Super Cycle, has been our mantra.

For trader types, the main question now is when does the four-quarter pullback end and the next upward move begin? Global oil demand trends remain constructive, obliterating the "peak demand happened in 2019" crowd and, so far, overcoming economic uncertainty in the three largest oil consuming areas—China, the United States, and Europe. While we see the ability for Permian oil supply to grow for several more years, a growing debate as to its eventual peak year is more legitimate than the debates about oil demand peaking any time soon. As such, we continue to believe a new CAPEX cycle will be required and we will need incremental oil supply beyond US shale.

What has always excited us most and we believe is the critical long-term issue facing traditional energy is the potential for structurally improved profitability. So far, the sector is passing with flying colors the important test of retaining improved ROCE despite sequentially lower oil prices. Greatness is revealed at cycle troughs by earning cost-of-capital (or better) returns at a normal trough or at least break-even at a deep trough. While $70-$75/bbl oil does not feel like a classic trough, oil prices have been cut nearly in half and the sector is still earning mid-to-upper teens ROCE. Ultimately, companies that generate competitive ROCE over the long run and return excess cash to shareholders we believe will prove irresistible to investors, even if the path higher is a rocky one.

Our core views at the mid-point of 2023 remain broadly unchanged:

We continue to believe we are now in year three of what will ultimately prove to be a decade-plus period of structurally improved profitability for traditional energy after the 15-year downturn from 2006-2020.

We see global crude oil and natural gas demand (and for that matter coal as well) as on-track to grow at least into the 2030s. It is possible demand for traditional energy sources could grow well beyond the 2030s in the event that other developing countries can follow in the footsteps of the legacy Asian Tigers and more recently China in meaningfully improving economic opportunity. India and Africa stand out as key regions to watch followed by Latin America.

We believe transitioning to a healthier energy evolution from the current messy energy transition requires a strong and growing domestic oil and gas industry in the United States, Canada, and ideally Europe, though we remain skeptical on the latter due to extreme "climate only" ideology that dominates in Europe.

We believe that structurally improved profitability and competitive dividend growth will help the traditional energy sector return to a double-digit weighting in the S&P 500 before this cycle ends.

Five big questions at the mid-point of 2023

(1) When will the Permian Basin peak and the steepening global oil cost curve lead to a global supply crunch?

My former colleagues at Goldman Sachs recently published the 20th edition of their Top Projects report series, which has long underpinned our view of non-OPEC oil supply—both during and since my time at Goldman Sachs. Notably, for the sixth straight year, the oil cost curve has steepened (Exhibit 1). A supply crunch is coming, which we believe will necessitate a new major projects CAPEX cycle.

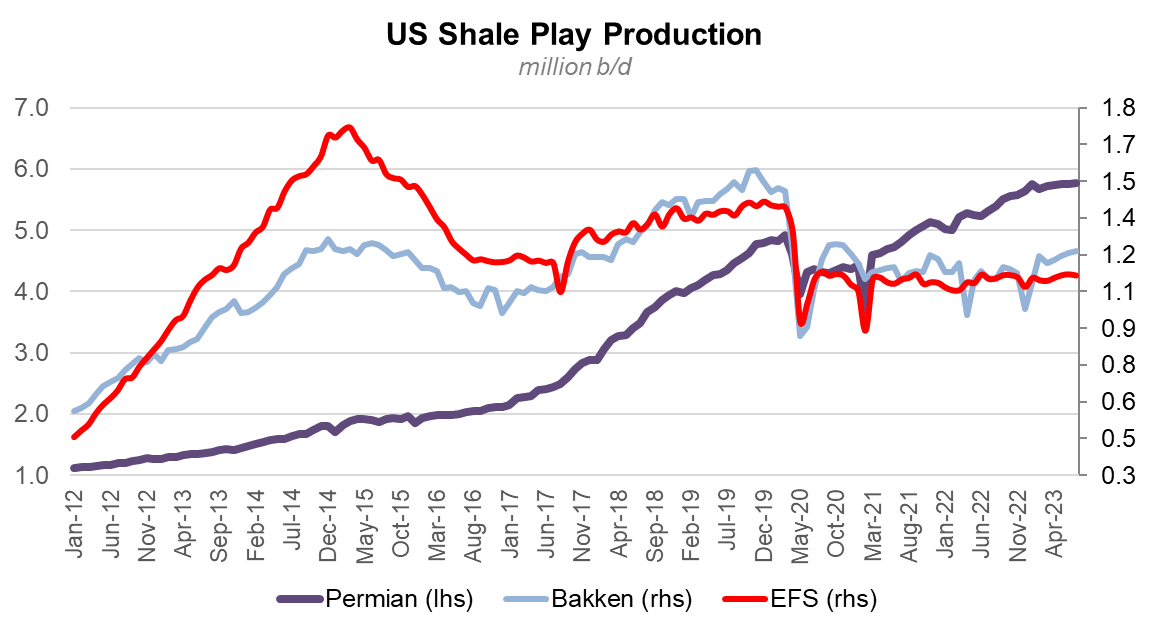

With US shale representing around 70% of global oil supply growth last decade (pre-COVID), the maturation of US shale is the key area to watch. Both the Bakken and Eagle Ford stopped growing several years ago, leaving the Permian Basin as the core US growth engine (Exhibit 2). The question therefore is: When will Permian production peak and will it enter a long-term plateau or fall off more quickly post peak?

We believe "peak Permian" is still several years away and therefore a transition from "Super Vol" to "Super Cycle" is a premature call in July 2023. We also believe a long-term plateau is far more likely than a peak followed by sudden decline. We would peg "peak Permian" as more likely to occur in the 2026-28 time frame consistent with Goldman Sachs and Enverus projections. Our views are based on our interpretation of various public and private research, data, and analyses.

Exhibit 1: Per GS Top Projects report, oil cost curve steepened in 2023 for sixth straight year

Source: Goldman Sachs Research.

Exhibit 2: Permian growth expected to slow, suggesting peak US oil shale may be nearing

Source: EIA.

(2) Is $70-ish oil and 15%+ ROCE really a trough?

While the traditional energy sector looks inexpensive on a variety of valuation metrics that reflect current strip pricing and expected profitability, we recognize that the idea that a cyclical sector can trough at a mid-teens ROCE seems naively optimistic. When companies are losing $ billions and are very out-of-favor, the "we are at trough" call is more easily accepted.

While we too would not instinctively characterize mid-to-high teens as a "trough" ROCE, the fact that the underlying structural trend remains positive and considering the extended period of below-normal ROCE in the 2010s, we increasingly think we are within shouting distance of the short-term low for the sector (Exhibits 3 and 4). We would note that in 2018-2019, we would not have thought that 10% sector ROCE was a near-term peak, as it turned out to be.

When ROCE is structurally declining as it was over 2006-2020, lower highs and lower lows are the norm. In a structurally improving trend, higher highs and higher lows should similarly be expected. Clearly, 2020 marked a generational deep trough that we do not place any odds on returning to any time soon. Even if we had a 2008-styled deep global recession and corresponding oil price collapse, we believe sector profitability would be considerably better than what occurred in 2020. Therefore, we see little value in waiting for the end of the world to reappear. It's going to feel unsettling as it does now. In a structurally improving profitability trend, the near-term troughs are more likely to be less dramatically awful than when the structural trend is headed down.

Exhibit 3: ROCE adjusted for oil prices remains structurally improved

Source: S&P CapitalIQ, Veriten

Exhibit 4: In 2018-19, a 10% ROCE did not feel like a peak then, but we were still in structural downtrend

Source: Bloomberg, S&P CapitalIQ, Veriten

(3) Is Super Vol a better macro backdrop for traditional energy equities versus a Super Cycle?

Portfolio managers, analysts, corporate executives, and board directors all instinctively decry volatility. We take the opposite view: volatility can be your friend, especially when almost everyone either wishes it away, or, worse, ignores it.

We increasingly suspect that high levels of realized and expected volatility are keeping companies cautious and CAPEX constrained, certainly more so than if we were in an obvious super-cycle analogous to 2002-2014. Yes, a super cycle sounds like it would be better than a Super Vol macro backdrop for traditional energy companies. However, the experience of 2002-2014 shows that it was only "better" through 2006, the year sector ROCE peaked (Exhibit 5). The last 8 years of that era resulted in a dramatic erosion in profitability due to a massive jump in CAPEX. That is not a history worth repeating.

Exhibit 5: The last super-cycle ultimately proved destructive for sector ROCE

Source: Bloomberg, S&P CapitalIQ, Veriten

(4) As US shale matures, will investors return to those companies with non-shale skillsets?

One could argue this is a twist on the diversified versus pure-play question from our January 2023 post. But in this case we are asking a slightly different version of the question. With the uber-focus on domestic shale and in particular the Permian Basin, companies with assets and skillsets in other areas, including Canada (oil sands, Montney, Duvernay), offshore, or overseas have generally been left for dead by most investors. We believe it is worth doing the work to understand the quality of management teams and asset bases for the non-Permian, non-shale producers. It may be premature and it's quite likely that non-shale E&Ps have their own challenges. But we would recommend spending more time on a broader universe of traditional energy companies. It will soon no longer be just about the outlook for US shale.

(5) Will US and Canadian energy policy evolve to recognizing the critical role it can play in meeting Rest of World energy needs?

Under our broad theme of "The Energy Transition Needs to Transition," we see a major opportunity for US and Canadian energy policy to divorce itself from European-styled "climate only" ideology and instead focus on how American and Canadian traditional and new energy can help the Rest of the World meet its energy needs.

We (USA + Canada) should be looking to increase our exports of crude oil, refined products, and LNG to the Rest of the World and provide a counterbalance to export growth from the Middle East and Russia. We have previously articulated a pathway to a net 10 million b/d of oil exports from the USA + Canada (see Exhibit 6). LNG exports in the United States are already on-track to grow meaningfully; Canadian LNG exports should also be part of the global solution.

We also have the opportunity to drive growth in new energy technologies which will be critically needed if billions of people are to benefit from improved living standards we take for granted. Between our capital markets, our culture of innovation and competition, investments spawned by the Inflation Reduction Act, our technology sector, and our sizable energy sector, the United States along with Canada have a lot to offer the Rest of the World.

Exhibit 6: A path to 10 mn b/d of net exports from US + Canada

Source: IEA, Veriten

Revisiting the five big questions we asked at the start of 2023

(1) If oil prices and ROCE fall in 2023, does it mean the structural ROCE upcycle is over?

January 2023 view: No, so long as ROCE vs oil prices stays "above the regression line."

July 2023 update: So far, so good. Structural ROCE trends remain favorable even as cyclically oil prices have weakened (Exhibit 3).

(2) In a world that favors ROCE and dividends, is a diversified E&P business model preferable to being a pure play?

January 2023 view: Yes, in many cases.

July 2023 update: Our view remains "yes, in many cases" (there are notable exceptions), but significantly more time will be needed to make a definitive conclusion on whether a diversified versus pure-play business model will be better.

(3) How can an E&P company add duration and diversify without upsetting investors in the short term?

January 2023 view: It's tricky, case specific, and may not be possible...i.e., it may not be possible to not upset investors.

July 2023 update: We think the January 2023 answer accurately anticipated how 2023 deals have been received—a mixed bag and case specific.

(4) What does $TSLA's valuation correction mean for EV growth projections?

January 2023 view: There will be growing recognition in 2023 that a 100% EV future is a pipe dream, no matter how many decades in the future one looks.

July 2023 update: Tesla shares have rebounded sharply from its beginning of year lows. Despite the momentum, we do note some moderation in the tone from other auto manufacturers on the timing of their own EV ramps. From a macro perspective, there is no change to our base-case view that EVs will experience significant growth in coming years but fall well short of the hockey stick projections for near 100% sales by the mid-2030s. However, we would acknowledge that not enough has happened in the first half of 2023 to cause the broader market to have more doubts on the hockey stick projections.

(5) Does the ongoing retreat of European financials from traditional energy matter?

January 2023 view: Yes in the short term, No in the long run.

July 2023 view: The abrupt collapse of the Net Zero Insurance Alliance is a step in the right direction, but doesn't change broader concern that mis-guided "climate only" ideology will lead to reduced involvement from European insurers and banks in traditional energy. The broader Glasgow Financial Alliance for Net Zero (GFANZ) still exists. That said, we would observe that the intensity of the exodus trend has slowed, and there is at least somewhat greater hope relative to earlier in the year that the worst effects from organizations like GFANZ can be overcome.

⚡️On a Personal Note: Top Projects

I would like to congratulate my former colleagues at Goldman Sachs on the 20th edition of the flagship Top Projects series. I was there for the original Top 50 projects report and the next 10. Anthony Ling, a now retired partner who was the lead analyst for European Oils and led the global oils team in that era, deserves credit for its creation. His new junior analyst at the time that did a lot of the underlying work was none other than Michele della Vigna. Congratulations to my friend Michele on 20 years at Goldman Sachs!

The Top Projects report series remains the key underpinning to our oil supply work, in particular for non-OPEC production. In the early 2000s, it was observing the delays and disappointments with our original forecasts in those early reports that ultimately was a major driver of our March 2005 Super-Spike call.

All Street analysts build models and have forecasts. It is always surprising at how few back-test what worked and what didn't in order to learn from mistakes and errors. Reconciling the miss in our expectations for robust non-OPEC supply growth in the early 2000s revealed project slippage, and, critically, increased declines in non-modeled production (i.e., base declines). After nearly two decades of consistent unit cost deflation, costs had suddenly begun to tick up. The long-term cycle had turned. It drove a career call and ultimately led to the creation of Super-Spiked!

⛳️ The Un-Retirement Blog: Episode 4

The start of 2H2023 seems like a good time to give an un-retirement progress update. Everyone's home from college. Our golden doodle is complaining that her favorite couch spots are not available. Our youngest successfully passed her driving test. No more babies left needing to learn parallel parking!!!

Critically, it's been a good golf season so far. Winter rust is mostly shaken off...just need to shave a few strokes from green-side rough and we'll be back to peak form. Thank you to our club pro J.T. for eliminating my old-man slice last year. He has defied physics. I am smashing my drive further and better at age 54 than when I took up golf at 45.

Through June 30, I have played 36 rounds in 2023, which puts me well on-track to achieve the un-retirement goal of 60-65 rounds in 2023. One round on the weekend, an early morning or late afternoon round on a weekday, and a family/spouse nine holes is not a problem at Veriten. I would not have dared to have attempted the pursuit of such leisure during my Goldman years. I am getting soft.

1H2023 un-retirement golf highlights:

Played Winged Foot for the first time at an MGA charity event.

Played in a pro-am event with LPGA professionals ahead of The Chevron Championship at the Club at Carlton Woods in The Woodlands.

Made the shoot-out with my partner at our club's premier member-member event over Memorial Day weekend. I had a memorable chip-in from the back of the green to make it to what effectively became the semi-final round of the shoot-out (Exhibit 7).

As expected, my GHIN backed up its usual three points at the start of the year rising to a soft cap of 10.8 from 7.8 at the end of last season (posting ends in November in the US Northeast and starts up April 1). I am now back headed in the right direction, with a current 9.9 GHIN.

Low round for the year, thus far, was an 80 at Lundin Golf Club in what was the last of four glorious early May rounds in the Kingdom of Fife. I look forward to heading back to St Andrews in September around my annual talk at the Oxford Energy Seminar and may try to sneak in an extra visit in late August.

Perhaps most remarkably, I won 3 of 4 June rounds against my 19-year-old 4-6 GHIN son (I received 5 strokes). He owes me three beers and I owe him one (we went with a gross payments approach, rather than net wins). Note: the legal drinking age is a sensible 18 in the United Kingdom which is where we will settle our beer debts. UK energy policy may leave a lot to be desired, but an 18-year-old drinking age is a total no brainer, especially for college kids. It is a considerably healthier and safer environment than what I would observe on US college campuses.

Exhibit 7: Celebrating a challenging, downward sloping chip-in from behind the green to make round 2 of the shoot-out of our club’s flagship member-member

Source: The Putter

🎤 Streams of the Week

I appeared on two podcasts that were published this past week, including Gulf Intelligence’s Half-Time Talk and Robert Bryce’s Power Hungry Podcast. You Tube links to each are below.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Good stuff as always Arjun! A couple of real points of interest. 1. While Permian peak is further out, that still means growth for E&P has to come from somewhere else (only so much consolidation will do without ability to add net new geologic resource). If growth is your objective, then you need to navigate the diversification pathway which as note, will cause some investor rotation. 2. Diversified play in E&P--you mean different basins/regions versus integrating further down the value chain? For me, I wonder if there is more room to run in the GOM. Unless we have some major shift in geopolitics I assume LATAM (Brazil, Mexico, Venezuela) is challenged which is why you focus on Canada? What would have to happen to have companies return to those regions? Do you think the time for foreign shale reserves is finally nigh?--Argentina, China, Russia. 3. What about asset light integration? Supply chain JVs with upstream and global midstream/downstream players with low access to reserves?

Regarding the Permian and shale recovery in general, Darren Woods said at the Bernstein conference that XOM only get's about 10% recovery in shale right now but they think they can double that. If XOM can really double recovery will that have a significant effect on supply, i.e. would they license that tech to other companies such that most shale production can double recovery?

https://seekingalpha.com/article/4608790-exxon-mobil-corp-xom-bernsteins-39th-annual-strategic-decisions-conference-2023-call