Reframing the growth versus returns trade-off debate

Corporate Strategy

"Growth" versus "returns" is a long-running debate among management teams, investors, and other industry observers. It is a question that is again starting to percolate in discussions with a broad range of participants, including policy makers, academics, industry executives, and investors. We declare unequivocally that we reject the premise of the question: there is not a choice to be made in terms of focusing on profitability (i.e., "returns") or volume growth. The sole purpose of an enterprise is to generate profits by selling goods or services society demands. It's always and only about long-term profitability. Full stop.

The better phrasing and what many may actually be asking is how fast can or should a company grow, while still aiming for top quartile profitability versus the sector and the S&P 500 over the long run. Long-lived projects in particular can require several years of upfront spending before start-up and the generation of earnings/cash flows. We do not characterize such projects as prioritizing growth over returns. Rather, they shift risk/reward to one of long-term returns potential and sustainability with the risk being unsuccessful project execution or a meaningful change for the worse in broader macro conditions (or both). It's an important distinction. The focus is always on profitability; it is duration and execution & macro risk that is the trade-off. If we are being pragmatic, investors today are generally saying they do not want companies to take the execution or macro risk of engaging in long-cycle projects and they would prefer companies not ramp-up short-cycle drilling opportunities for fear of execution deterioration. In other words, investors do not believe most companies can grow faster and sustain the otherwise improved levels of profitability.

We would observe that for upstream companies in particular, an excessive focus on short-term shareholder returns maximization (i.e., dividends and stock buybacks) runs the major risk of being unsustainable over the long run as drilling locations are depleted. We can see this risk in real-time where various shale oil E&Ps have very different amounts of "Tier 1" inventory running room.

As we look out over the next 10 years, we believe:

there is no evidence that oil or natural gas demand is on-track to peak or plateau any time soon; in fact, we do not see how anyone can know at this time which decade let alone year we will see a peak, given the massive unmet energy needs that exist for the other 7 (soon to be 9) billion people on Earth that are not among the lucky 1 billion of us.

that US shale oil is unlikely to comprise circa 100% of future net global oil supply growth as it did last decade.

that there is significant power generation demand growth coming as the wider world becomes wealthier, as artificial intelligence and compute power sees exponential growth, and as electrification of some portion of transport and other non-traditional sectors steadily progresses; we believe natural gas/LNG will have a major role to play in meeting this growth.

As we look at whether something greater than 0%-3% per annum volume growth makes sense for individual companies, we would ask the following five questions:

Will a company be able to maintain mid-teens or better ROCE over a full cycle at higher growth rates, and if so, for how long?

Will a company earn at least a cost-of-capital ROCE (around 8%) at a normal trough and never lose money even in a deep trough?

If a company is not on-track to add future low-cost inventory, is it simply pulling forward the year by which its returns will fall off, and if so, by how many years?

If a new area is being pursued (e.g., exploration, global expansion, LNG, new energies), does the company have expertise or a competitive advantage in the new area?

Will the company avoid the CAPEX-driven "quadrilateral of death" seen last decade by the vast bulk of the sector?

Avoiding the "quadrilateral of death": Last decade's growth nightmare still looms large

Within especially the upstream portion of the traditional energy sector, the notion of a trade-off between growth and returns comes from the idea that during distinct periods of an upcycle, the E&P and oil services sectors would attract investors that favored top-line growth, with the presumption it would eventually lead to bottom line growth. By now, everyone knows that high levels of growth capital spending over 2006-2014 led to a collapse in sector profitability. It was a disaster for industry and investors, even as broader society benefitted from the flood of shale oil and gas via inexpensive energy.

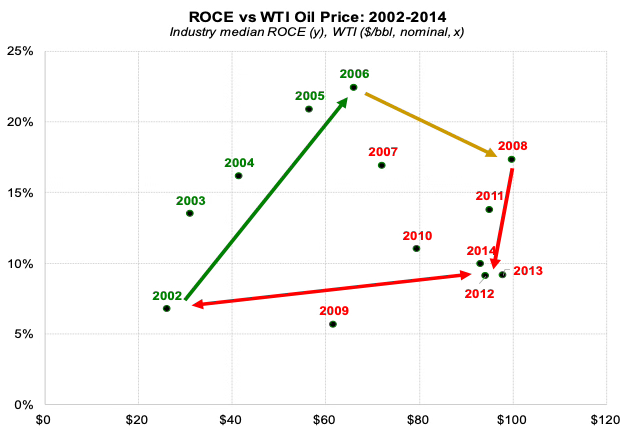

We have previously introduced the "quadrilateral of death" to show the detrimental impact of poorly executed capital spending during the last super-cycle (Exhibit 1).

2002-2006 (green line) was the sweet spot of the super-cycle as oil prices rallied from around $20/bbl to the $60s/bbl (all in nominal $ of the day) and ROCE rose in lock step.

2006-2008 (yellow line) was the warning that excessive CAPEX was beginning to erode profitability as oil prices rallied another $35/bbl yet ROCE actually fell slightly.

2011-2014 (red line) was the pure misery phase as ROCE collapsed during a time oil traded around $100/bbl. By the end of the period, oil prices had quintupled but ROCE was no better than it was at $20/bbl, an absolutely horrific ROCE round trip.

And then oil prices crashed, and a five year stretch of sub-cost of capital ROCE ensued. And then COVID hit, and things actually got worse.

Exhibit 1: Quadrilateral of Death

Source: Bloomberg, S&P CapitalIQ, Veriten.

Since the 2020 COVID collapse, investors have demanded that essentially all excess cash flow above maintenance CAPEX levels (defined as CAPEX to maintain flattish production) be used to either paydown debt or returned to investors via dividends and stock buybacks. We get it: the quadrilateral of death can never be repeated.

But the world needs energy. Someone is going to supply it. There is no reason US, Canadian, and Western European oil and gas firms should not be a major part of the mix. The world will be a safer and healthier place if western world oil and gas is profitable, healthy, and leaning into advantaged areas of future low-cost energy supply growth.

Going concern valuation uplift

Profitability in excess of cost of capital is a prerequisite to gaining "going concern" valuation status. "Going concern" valuation status means terminal value is not assumed to be zero; it is synonymous with multiple expansion. We note that achieving top quartile profitability on its own we do not think will lead to a "going concern" valuation premium. Given that secular oil and natural gas demand growth rates are low single digit at best, a traditional energy company will likely need to "take share" by investing in traditional or new energy areas that are growing faster than base demand. Furthermore, investors need to believe that advantaged profitability can be sustained over the long-run, which we will define as decade-plus running room. There are not that many companies that can declare they have decade-plus running room.

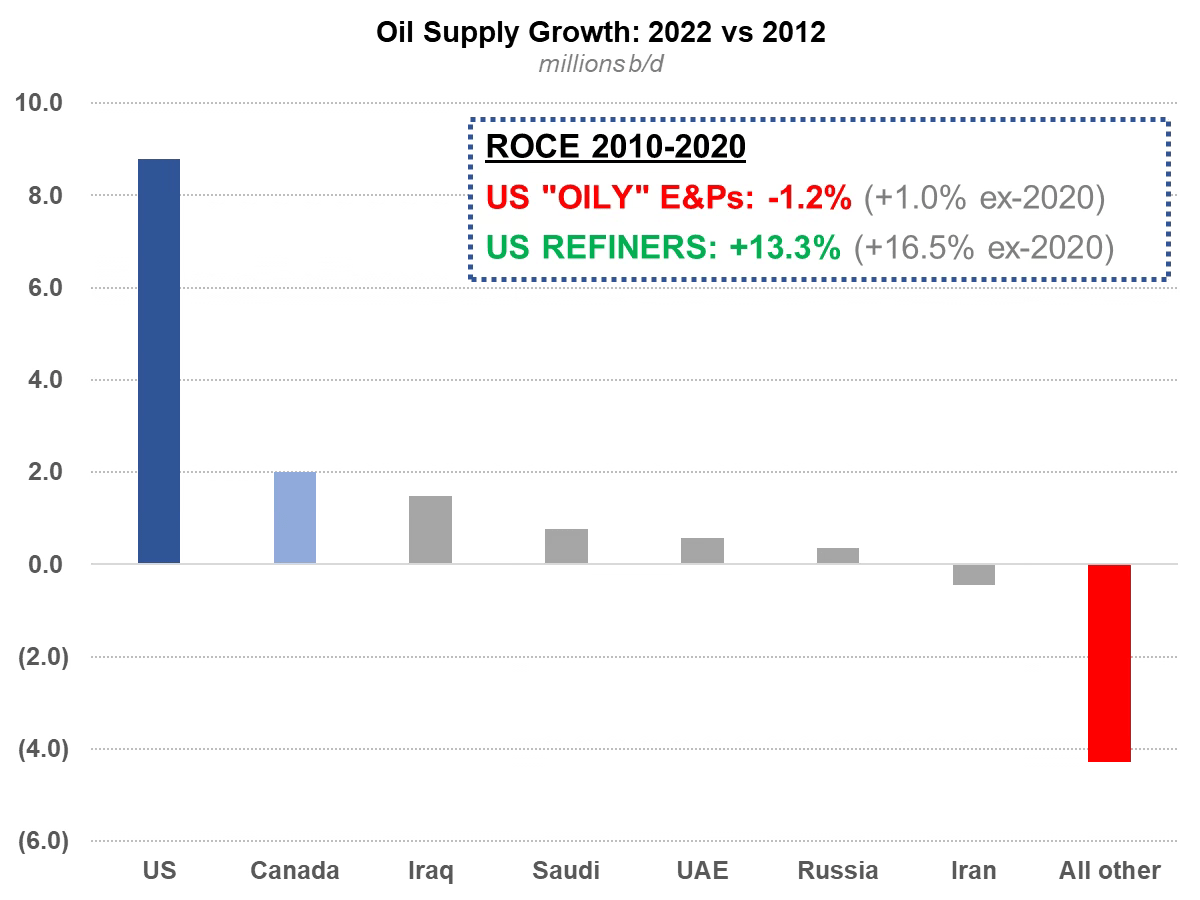

Last decade some thought that it was possible to gain share and demonstrate long-lived development potential via US shale oil. US shale oil volumes in fact boomed in the 2010s, accounting for essentially 100% of net global oil supply growth—a remarkable figure. Shale oil E&Ps took massive market share from oil producers in most other regions. Unfortunately, it translated into literally no profitability as ROCE averaged close to 0% for shale oil E&Ps in the 2010s. It turned out the refining sector was the traditional energy winner of the shale revolution (Exhibit 2). We are now at a point where historic aggressive drilling has depleted the quantity of advantaged locations for many participants...not everyone, but many.

Exhibit 2: Shale growth versus profitability

Source: EIA, IEA, S&P Capital IQ, Veriten.

Why have investors been so cautious to re-embrace the sector?

We see four main drivers of investor reluctance to embrace risk-taking by traditional energy companies:

Poor profitability seen over 2010-2020 (discussed above).

Near-term recession/weak GDP concerns in the three largest oil consuming regions of China, Europe, and the United States.

Long-term "energy transition" uncertainty and the potential for oil demand in particular to peak and either plateau or decline in coming years.

A Super Vol rather than super-cycle macro backdrop, as tight supply-side conditions bump against recession concerns; volatility is often inversely correlated with an investor’s (or company's) propensity to support long-term risk capital.

We have discussed our views on each of these points extensively in prior Super-Spiked posts.

Profitability: We believe profitability cycles are long-term in nature, 10-15 years up and 10-15 years down. We have just ended a 15-year downturn (2006-2020) and are in what we believe is Year 2.5 of a decade-plus period of above-normal profitability.

We agree that the near-term economic outlook is uncertain, which is the main reason we describe the current macro backdrop as "Super Vol" rather than super-cycle.

We do not believe oil or natural gas demand is on-track to peak or plateau anytime soon.

In our view, taking risks earlier in a cycle is more sensible than later in a cycle. It is subject, however, to the questions and framework we described in the opening section of this post.

Upstream: How fast to grow?

For upstream companies, we would include the following supplemental questions:

Has a company entered a new area via business development, M&A, or exploration that is driving higher growth?

If a company is merely accelerating activity in an existing, well-defined play, how soon will faster growth eat through remaining high-quality, low-cost inventory?

What confidence exists that we will not see execution slippage as growth spending is ramped up?

The main reason we think investors today are demanding that companies adhere to zero-to-low single digit volume growth aspiration is because companies have:

historically over-estimated how many years of truly "Tier 1" locations they actually held (i.e., high-quality resource life is generally overstated).

experienced cost inflation that raised break-even prices when targeting too high of a growth rate.

depleted their inventory of Tier 1 locations, effectively accelerating the day by which they would face the need to move to lower-quality areas or engage in M&A with an unknown cost and risk profile.

As a reminder, we define "Tier 1" acreage as having drilling locations that can justify investment at $60-$70/bbl WTI (or lower) in order to generate at least 8%-10% corporate-level ROCE. Many companies, especially those in the shale oil and gas business, made the mistake of relying on so-called "half-cycle" IRRs and a net present value (NPV) maximization approach, with the latter ultimately reflecting too low of a cost of capital relative to what investors require to ascribe "going concern" status to a company.

In our view, a framework for the appropriate growth rate will consider the duration by which a company can maintain the aforementioned profitability objectives for as long as possible. In order to achieve going concern status, investors will likely need to see articulation of something on the order of a decade (or more) of running room, with some confidence in the potential to continuously extend that decade via exploration, the application of new technologies that improve recovery factors, business development, or M&A. Said another way, five years from now, will there only be five years left or is there the potential for 7-10 (or more) of running room to remain.

Downstream: Feedstock and demand mix shifts is the opportunity and challenge

Unlike upstream companies, downstream assets are inherently long-lived though subject to the need for at times significant CAPEX to maintain and modernize a facility. Organic growth (i.e., excluding acquisitions) for refining companies typically means investments to alter the types of feedstocks it can process or to change the desired product yield. For retail marketing, it can be about building new stores or upgrading/improving existing locations.

The complexity of feedstock mix and refined product yields has meant that volume-based growth targets have never been a focus for investors. However, that is not to say that investments are either unneeded or not considered. As an example, when Venezuela heavy oil supply was increasing dramatically in the 1990s, there were organic investment opportunities to process the heavy crude and take advantage of the (volatile) discount heavy crude oils trade relative to light-sweet crude oil (the latter of which are easier to process and often yield superior amounts of preferred refined products).

During the shale oil revolution of last decade, which coincided with declining heavy oil supply from Mexico and Venezuela, investments were needed in infrastructure to take advantage of discounted onshore light-sweet crude oils versus corresponding offshore grades. In other words, downstream "growth" CAPEX is usually about being able to take advantage of the margin (or spread) opportunities that arise from supply/demand changes to feedstock or product yields.

⚡️On A Personal Note: Oklahoma!

This past week I had the good fortune to join a panel on capital allocation at an "Energy and the Economy" conference co-hosted by The Federal Reserve Bank of Dallas and The Federal Reserve Bank of Kansas City held at The Petroleum Club in Oklahoma City. Oklahoma is not easy to reach from the East Coast. During my career as an equity analyst, we by and large cheered when companies invariably moved to or were acquired by companies based in Houston. But this was my second trip in three years to the Sooner state and like the prior time I was struck by how positive my visit was and in particular how nice and friendly everyone is in Oklahoma.

Flying commercial over Oklahoma

Source: Super-Spiked.

You might be thinking that since I live in the New York suburbs, the "what qualifies as nice" bar is set pretty low. And no doubt there are plenty of friendly people in South Carolina, Texas, Vermont, and many other places outside of the Tri-State area (NY, NJ, Connecticut). But I would say Oklahoma takes niceness to a higher level. Even the people at TSA are friendly and polite! The breakfast waitress at the hotel stopped by about 15 times to refill water or coffee, check on the food, give me updates on the timing of the arrival of my meal, and issued no less than three apologies for the toast taking an extra minute to come out. Great service! She was focused on doing her job well; not scrolling her cell phone at work.

When I was at Goldman, I recall receiving a phone call from the office of the Lieutenant Governor of Oklahoma following the news that Phillips Petroleum and Conoco were merging and would relocate their headquarters to Houston. The question posed was: "How can the Wall Street community help keep the merged company in Oklahoma?" I have no idea what the person thought any of us in New York could individually or collectively do to keep a large oil company from moving from Oklahoma to Texas, or why any of us would want to stop such a thing from happening in the first place. There were no direct flights in those days to OK City or Tulsa let alone Bartlesville; in New York, we don't do connections. There are nearly hourly flights to and from Houston; we supported the move.

I have to say that my bad attitude about connecting flights to Oklahoma still holds; it's simply not easy to travel to if you don't live in Texas and have to fly commercial airlines. But over a 30-year career, I am not sure I've had a bad experience in the state. Here are my Top 5 visits to Oklahoma in chronological order:

Bartlesville, circa 1993: Phillips Petroleum analyst meeting

My first ever analyst meeting was with Phillips Petroleum to visit its Sweeny (Texas) refinery followed by a day of presentations at its Bartlesville headquarters. My first ever visit to an oil refinery started with a lengthy safety discussion. That very strong safety culture persists with both successor companies to this day. I remember Mark Gillman, a veteran analyst with a strong reputation for challenging management teams, asking the Sweeny refinery manager why he was spending so much time on safety. (paraphrasing) "If we don't run our assets well and keep our people safe, we will never sustain acceptable levels of profitability." Amen.

The flight from Sweeny to Bartlesville was my first ever private jet (PJ) experience. I will say that whatever plane Phillips was using in 1993 still beats the commercial flight options to Oklahoma today a million times over.

In Bartlesville, we stayed at the one and only Hotel Phillips. While not a Four Seasons by any stretch, it was a perfectly acceptable experience. Phillips' legendary and long-time investor relations head Ed Grigsby ran a fun late night poker game in an upper floor suite.

Ardmore, circa 1994: Noble Affiliates company visit

My first boss to whom I owe significant thanks for getting my career off to a great start was Paul Leibman of Petrie Parkman & Co. Paul, myself, and Mark Baskir of Neuberger & Berman traveled to Dallas to visit Maxus Energy and Oryx Energy, two deep value E&P names that I recall offering significantly greater entertainment, rather than shareholder, value as a covering analyst in the early 1990s. We drove from Dallas to Ardmore, Oklahoma for a visit with the CFO of Noble Affiliates, whose name I believe was Bill Dickson.

Upon arriving at Noble's headquarters, we were met with a sign at the front door: "Out to lunch, back at 1 pm." A second note indicated we should meet Mr. Dickson at a local lunch spot that I recall serving barbeque chicken. As a reminder, this was the pre-internet, pre-mobile phone era.

It was a great lunch and a terrific visit with Noble. Mr. Dickson would easily make a Top 10 list of the nicest, most decent energy sector executives I've interacted with. He must have been born and raised in Oklahoma.

OK City, early 2010s: Visiting Aubrey at Chesapeake HQ

I don’t believe I was ever the lead analyst that covered Chesapeake Energy, but had plenty of interaction with its late, legendary founder Aubrey McClendon. If you were a Wall Street analyst covering Chesapeake, by definition you were going to have a love-hate relationship with Aubrey. Aubrey ran his company at Mach force, and it was simply not possible as an analyst to always be excited about whatever high-risk, high-potential move he had just made. As someone running an energy research business unit and a Goldman partner, Aubrey would make clear to me the times he wasn't happy with Goldman's coverage (his style was the opposite of the approach John Hess took with analysts, which I discussed two weeks ago).

On one such occasion, I did offer to go out and visit the company to hear first-hand whatever his plans were at that time. Chesapeake had an amazing, college-like campus. What I remember most is that wherever we went, Aubrey knew every single employee's name. To a person, he received a hello at a minimum and in most cases a hug. We were grabbing a bite to eat in the cafeteria at an off hour and the cook came out to thank Aubrey for his help. I don't know what the details were, but the person was clearly deeply appreciative of whatever Aubrey had done to help him or his family. While the trip did not change our view of Chesapeake’s plans at that time, it did change my view of Aubrey. He was clearly loved by the employees I came across.

This post is ultimately about risk taking. None of us are perfect human beings and neither was Aubrey, at least not as a CEO. But he was a risk taker. He is as responsible as anyone for helping commercialize the US shale gas boom. The traditional energy world would benefit from at least a small dose of Aubrey's risk-taking mentality to find its way into more leadership teams today.

Aubrey McClendon

Source: Oklahoma Hall of Fame

OK City, June 2022: Presentation at E&P company Board meeting

I'll keep this one briefer and generic since it's a contemporary situation, and I'll protect the innocent (i.e., me) by not naming names. But I was invited to speak in Oklahoma City at a Board meeting for a non-Oklahoma-based E&P company. After starting Super-Spiked in November 2021, I was pleasantly surprised to see company managements that I had not interacted with as a Goldman analyst subscribe.

The engagement at this particular board meeting was a lot of fun and I consider it a key catalyst to ultimately motivating me that it was time to un-retire and join Veriten. Veriten's business model represents 100% of the things I enjoyed doing as an analyst—and this meeting crystallized that for me—while having almost none of the things I would rather do without. The one item that unfortunately has not changed is that as a Goldman research analyst you flew commercial; that is also true at Veriten. Maynard, we need a Veri-Plane!

OK City, November 2023: Dallas-K.C. Fed Meeting

It was my honor and privilege to join the aforementioned "Energy and the Economy" event jointly hosted by the Federal Reserve Bank of Dallas and the Federal Reserve Bank of Kansas City. The folks from the Federal Reserve banks were terrific and welcoming. It was a really great audience, a pragmatic discussion, and it was in the Sooner State!

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue

You need to copyright quadrilateral of death.

Dan Jenkins wrote a great book about Texas but called it Baja Oklahoma

Energy companies need build business models that are able to withstand the volatility of the commodity cycle. To regain the trust of energy sector investors, financial discipline has to become a way of life.

The managers need to think like owners. The best test is to adopt consistent annual cash distribution increases as the measure of success. The business model should have a margin of safety. Too much leverage puts the distribution at risk. Maintain a fat distribution coverage ratio so distributions can grow when business is slow. Don't pursue business-trend fads that destabilize finances.

P.S. I love what you are doing with your website and podcast. And I am a regular listener of C.O.B. Tuesday. Keep up the good work.