Will AI Be Our Salvation Toward A Healthier Energy Evolution?

AI & EnergyGPT

For the first time since Super-Spiked’s creation in November 2021, we see “green shoots” that the world may be ready to evolve to a healthier energy evolution from what has been a “messy energy transition era”—our inspiration for starting Super-Spiked. The artificial intelligence (AI) revolution is here and with it comes substantial future power generation needs that is already exposing the shortcomings of what we have called a “climate only” energy investment and policy view of the world.

AI is a tangible catalyst to accelerate the move to “all of the above” energy investments and policy in the United States most notably, but possibly other rich countries that have heretofore made lowering carbon emissions the overarching driver of energy policy to the detriment of energy reliability, affordability, security, and, ironically, the environment and climate as well. The new growth driver of AI plus the imperative to meet the massive unmet energy needs of the other 7, soon to be 9, billion people on Earth that are not amongst The Lucky 1 Billion of Us point to significant opportunities for companies that are leaders in the technology, industrials, and energy sectors.

In this inaugural “AI and EnergyGPT” post, we use the popular Q&A style to provide our top ten initial perspectives on how growth in AI is relevant to the energy sector and why we see this as a catalyst to moving to a better energy policy backdrop.

(1) What does AI have to do with the energy sector?

Reliability and affordability are rightfully returning to being the dominant drivers of power generation capacity growth. The sizable expected power needs from the advancement of AI is already revealing the shortcomings of the “climate only” narrative that became mainstream around 2020 and over-emphasized intermittent renewables as the means to addressing climate concerns. Hyperscale data centers require 24/7/365 power generation, not occasional power when solar radiation or wind speeds are sufficient. It’s not a close call on this point and it is not a knock on solar or wind, which have a role to play in our power generation mix. Rather it’s a critique of policy makers positioning renewables as the be all and end all of how to meet energy needs with reduced carbon emissions. The public was never on-track to tolerate temporary power; the return of upward sloping load growth in the United States will ultimately drive policies that support “all of the above” power generation sourcing and grid modernization.

(2) What technologies will help balance inevitable renewables growth?

Nuclear and natural gas have major roles to play in a healthy power generation mix and are the big winners of AI-driven power demand growth; Big Tech is starting to recognize this reality. In our view, US and Canadian natural gas producers would be well served to ensure domestic resources are bulletproof on the methane issue, as we expect Big Tech to remain conscious of sustainability concerns.

China, India, and other developing countries are clearly on-track to use rising quantities of coal for the foreseeable future. The degree to which rich countries can help the developing world limit its future coal usage and instead utilize nuclear and natural gas for dependable power is a major opportunity in terms of both trade benefits and lowering carbon emissions. It should be a no-brainer uniting theme for both left and right and those that favor strong “climate action” as well as those that believe “climate alarmism” is at play.

(3) Where is Big Tech in its understanding of global energy systems?

We can see Big Tech starting to recognize that feel-good “net zero by 2050” promises never reflected the complexity of our global energy system nor their substantial role in creating products and services that are major drivers of energy demand. Tech-driven energy demand growth is a good reminder that oil and gas companies create essentially zero products that use the energy they produce; rather, oil and gas is a critical underpinning to all aspects of our massively improved living standards and societal wealth relative to the pre-fossil fuel history of the world.

There is a need for all non-energy sectors, consumers, and policy makers to deepen their knowledge of the realities of our complex, global energy and climate system and to not rely on single-issue narratives being pushed by some politicians and policy makers. We credit Meta (formerly Facebook) for adding John Arnold, a veteran natural gas trader who is now a thoughtful energy commentor, investor, and advisor, to its board, a clear sign that Big Tech understands it needs to ramp its own energy literacy. The demand for objective energy expertise across the global economy has perhaps never been higher, especially given the need to incorporate sustainability objectives is not going away even as it is not a primary objective.

(4) What opportunities exist for traditional energy to partner with Big Tech or Big Industrials?

Traditional energy companies have a major opportunity to get back on their front foot by laying out strategies that help meet the substantial energy needs that exist. As for the AI-driven power demand component, we think most observers will recognize that the oil and gas sector (integrated, upstream, midstream, and downstream) have not historically had very much by way of involvement in power generation. The questions we pose looking forward include:

Should the oil and gas sector look to diversity into power? Our instincts tell us it will be a challenge that would likely be met with significant investor skepticism. Still, we think it is worth at least exploring the subject.

Is power sector diversification more logical for US or Canadian natural gas producers? No one, including us, has previously advocated for diversification into ammonia or petrochemicals. Is growth in AI-driven power demand in an era where sustainability metrics have taken on greater importance different?

What opportunities exist for traditional energy companies to partner with Big Tech or large industrial companies, which are clearly seeking help to ensure reliable, affordable, and, ideally, lower emission power?

Would joint ventures or other non-traditional corporate structures be an avenue to participate?

Would it be more logical for a midstream or downstream company rather than an upstream producer to think through the opportunity set?

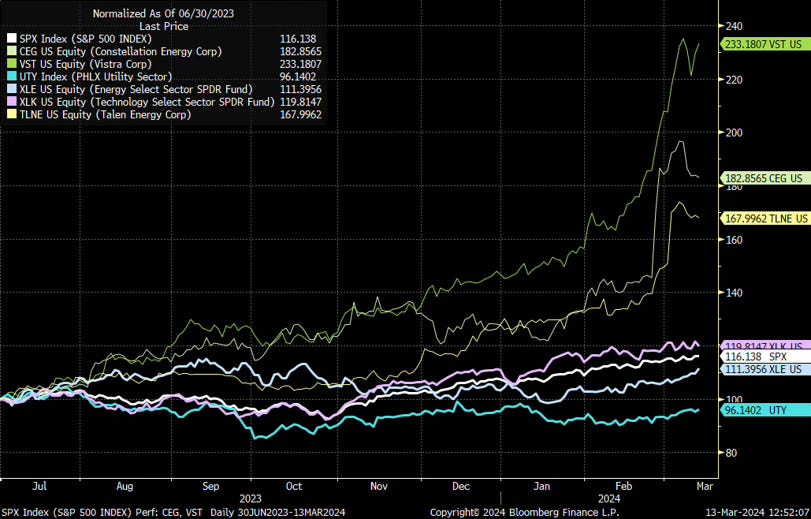

With power reliability a growing concern in the United States due to the growing share of intermittent energy sources along with renewed load growth, we see the business community taking steps to ensure their own power is reliable and affordable, first and foremost, and hopefully lower emission. Distributed, or perhaps dedicated, power generation will likely be considered by the largest companies. We see Amazon’s recent announcement to acquire a data center campus located at a nuclear power station in Pennsylvania from Talen Energy as the first of what will likely be many steps from Big Tech, and in the future Big Industrials, to ensure key investments have secure power (Exhibit 1).

Exhibit 1: TLNE shares along with CEG and VST have outperformed the Tech sector (XLK), Energy (XLE), Utilities (UTY), and the S&P 500 (SPX) since June 2023

Source: Bloomberg, Veriten.

(5) What impact will AI-driven power demand growth have on commodity price volatility?

There is no change to our Super Vol macro backdrop and mindset. To the extent desired load growth further diminishes spare capacity cushions, and given the growing intermittency embedded in power markets as renewables increase their share of capacity, broad-based commodity price volatility is likely to remain high. Bullish sentiment toward power generation and a complete lack of societal tolerance for blackouts or brownouts, means investment will come to solve the problem. It is just a matter of time, and we believe it is early days.

Note: This notion of a long-term investment cycle ultimately being the cure for a commodity bull market is the basis for our term “super-spike.” The super refers to duration; spike implies the bull market will not be perpetual.

(6) Will AI mean more compromise on energy and climate policy fights and less policy extremism?

No, that is not necessarily what we are saying. Climate versus anti-climate being the main parameters of disagreement is what we would hope will change. The idea that energy sources are partisan (referring to a US context in this case) has always been bizarre and unnecessary. Renewables should not be associated with Democrats and fossil fuels with Republicans; same thing with electric vehicles, heat pumps, and a host of future technologies. Both sides suck have room for improvement on the messaging.

Our preferred energy and climate policy framing would be the degree to which the government versus markets help address our areas of need and overcome challenges, and our view is you will need both. Markets typically do not address negative externalities such as pollution. Governments, as represented by a relatively small handful of elite decision makers, is a far worse allocator of capital than markets, the latter of which reflect the views and actions of the billions of people on Earth.

(7) Will AI finally kill ESG and other sustainability objectives?

We see AI as catalyzing a needed expansion in the definition of what counts as being “sustainable” rather than killing the concept outright. We believe broader society as well as the investment community will continue to ask companies across the economy, including traditional energy, Big Tech and Big Industrials, to articulate a pathway toward decreasing the carbon intensity of output, the products they produce, or the energy they directly or indirectly use. Fading “climate only” is not code for “drill, baby, drill” as the sole answer to meeting AI and developing world energy needs.

We believe California’s Big Tech behemoths, along with large Industrial consumers of energy, will face considerable pressure to articulate and implement sustainability attributes that mesh with AI growth. Trade-offs are inherent to the process of delivering economic growth that recognizes sustainability considerations. In our view, Big Tech is much better positioned than traditional energy companies to convince the public and policy makers of the importance of constructively working through the tradeoffs. Importantly, we believe Big Tech will find a lack of reliable or available power to be intolerable; it will sensibly force the issue of moving to a healthier energy investment and policy backdrop.

(8) But aren’t renewables the cheapest form of power generation?

The obsession by some, either explicitly or be inference, to promote “more renewables, faster, and sooner” as the over-arching theme of energy and climate policy has always seemed absurd to us. The renewables push usually comes with the false statement that renewables are now clearly the least expensive form of power generation. The statement is inaccurate in that no energy source or technology in any absolute sense is THEcheapest in all circumstances.

Take the Permian Basin as an example. There is acreage and zones that are very low on the global oil cost curve. There are other parts of the Permian that are high on the cost curve. This is true in essentially every oil and natural gas basin that contains at least some acreage that is at the lower end of the cost curve. Nothing in energy can be declared as THE low-cost solution. There is always a slope to cost curves.

This is obviously true for solar and wind generation. Solar radiation and wind speeds are clearly different around the globe. Why would Germany or New York state think solar and wind are reasonable replacements for nuclear generation? Very few deny the existence of intermittency with solar and wind. But there is a lot of fuzzy math on how it will be addressed in real time and on a cost-effective basis.

We suspect there are very few energy executives or experts that would reasonably disagree with most of our points. But that is not what you hear from those that prioritize climate above other issues. High profile statements like “we need to triple renewables capacity by 2030” are an example of mis-guided policy pronouncements by some of our most influential policy organizations. A better statement would be: “What are the mix of energy sources and technologies the world needs to ensure everyone can enjoy the living standards The Lucky 1 Billion of Us take for granted, while recognizing the need to address negative externalities related to climate and the broader environment?” It is too long and less catchy for sure. It is also the path we are headed toward.

(9) What is the role for renewables even if it isn’t a 100% solution?

Renewables have an important role to play in power generation. Once online, they represent “domestic” power that is not subject to external geopolitical disruption; we believe this will be attractive to countries that do not enjoy abundant oil or natural gas resources. Renewables also offer a distributed power generation opportunity that is not practical for every energy source. You can have a diesel-powered generator. But no one is going to have a distributed oil refinery or nuclear plant.

(10) Are you sure all this AI talk isn’t just hype?

We recognize that when non-tech analysts start commenting on a hot tech topic like AI, it is often a sign of a near-term peak in the hype cycle. That may well be the case! As readers know, we do not make stock calls so the very existence of this post should not be viewed as a contra-signal to sell NVIDIA shares. Of course, any weakness in the so-called Magnificent 7 would likely help fund flows into other sectors, including energy (Exhibit 2). But none of that is the point of this post.

It is our view that AI is the next big technology sector revolution. Unlike prior paradigms like the cloud or mobile, the incremental energy demand growth appears to be orders of magnitude higher for AI. Hence, we see AI progress as being highly relevant to how we think about the energy sector, both traditional and new energies.

If this post does in fact coincide with a Mag 7 peak, we will neither complain nor apologize. The world needs a healthy energy sector and the fund flows to support needed investments.

Exhibit 2: Since 2020, the market has been dominated by the so-called “Magnificent 7” with AI-driven NVDA the overwhelming winner

Source: Bloomberg, Veriten.

⚡️On A Personal Note: A career analyzing the most important sector in the world

The last day of March will complete my 32nd year analyzing the energy sector. It was by pure chance that I came to energy as I was a finance major at the University of Denver. A favorite professor of mine, Dr. Ron Rizzuto, recommended me to Petrie, Parkman & Co., and 32 years later I still find the sector to be absolutely amazing. It is global in nature; it is highly relevant at all times even when it is out of favor on Wall Street; it matters to everyone on Earth; and without it, life would unquestionably be much more challenging. And life is relatively more challenging for the other 7 billion people on Earth that either do not have access to energy or use significantly less energy than The Lucky 1 Billion of Us.

Everyone at all times has a view on the oil price. It matters to US presidents and their approval ratings. I have never heard widespread debates on the price of polypropylene. The fate of Starbucks coffee or Apple or even NVIDIA is not a driver of elections or geopolitical turmoil. No one wishes for geopolitical turmoil; rather it speaks to the criticality of energy that nations fight over it.

We often hear that young people today want to get into fields that have a purpose or mission, such as solving climate change or addressing social inequalities. All of those people should consider careers in the energy sector, both traditional fossil fuels or new energies. There is perhaps no greater calling in life that one can have than helping to ensure access to reliable and affordable energy. The use of energy near perfectly correlates with better overall environmental outcomes. The least fortunate in the wealthiest societies are significantly better off than their peers in poorer countries; hence the strong desire to emigrate to capitalist success stories like the United States from socialist or autocratic failed states.

Join an oil company or a new energies start-up. The cultures are different; one may be more to your liking. The one possible challenge with the fossil fuel industry is it is mostly in Texas and Oklahoma. If you prefer living on the US East or West Coasts, you may be better off in new energies. But if you want to experience different cultures around the world, there are a number of traditional energy companies with global businesses.

An alternative to joining an energy company is to analyze or transact in the sector on Wall Street or at a consulting firm. Here you will have a much greater freedom of choice on where you live. Come to the energy sector, perform well, and your expertise will ALWAYS be in demand.

🎤 Streams

MacroVoices podcast: This week Arjun appeared on Erik Townsend’s MacroVoices podcast (here). They discussed Arjun’s views about peak oil demand not being anywhere in sight, what, if anything, comes after US shale on the oil supply side, the timing and prospects of a new capital spending cycle in oil and gas, the prospect for a series of energy crises in the coming decade, whether Renewables and EVs can substantially dent fossil fuel demand, and the impact AI could have on energy transition narratives.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Very timely to kick off this discussion on the intersection of AI/Power and O&G. A couple of thoughts and questions. 1. Implicit in your commentary is that AI and all things digital are increasing the demand for more data centers. I love the term storage in the cloud but we all know at the end of the save button, there is a hardstack somewhere in Virginia whirring away for the next time you need that datapoint. Multiple studies show large increases in power needs across the country from industrial activity including data centers. We are at an interesting time in the utility sector for this surge in demand. Vast parts of the distribution and transmission infrastructure need replacement with assets decades past their sell by date. Reliability and affordability are lighting rod issues for the retail customer like you and I. As big tech and industrial customers move quickly to lock up "green" and reliable power, this puts more pressure on capacity to keep the lights on for the average voting public. I agree we will need more generation to come on the market but who should pay? If Big Tech Co XYZ locks up a 15 PPA at an attractive price, requiring new build generation by the regulated side of the house, should some of that be pushed back to industrial contracts? This is a big policy issue we will face. 2. On the ESG and sustainability point. I am hopeful that the convergence of AI/Tech and Energy will move us away from Carbon Tunnel vision when it comes to the sustainability discussion. Water intensity is a big issue, biodiversity, community, profitability, etc.. all need to figure into the definition of what constitutes sustainability for an enterprise. I think we will see this push the discussion past GHG emissions into a more holistic analysis. Look forward to more like this from you!

As always, a great write up, and you have not cursed the AI space by doing some much needed analysis!

How can anyone be so confident in the capex and growth plans of AI infrastructure without solving the power needs??

You are addressing the other side of the equation, and pointing out rightly that it's not a matter of renewables vs nat gas vs nuclear.....if the forecasts are correct, we need it ALL!!

I'm sure it didn't escape your notice that the NY Times and the Washington Post had big pieces on the topic this week.

Well done sir.