Market corrections, recession risk, and energy

Navigating the new Energy Crisis Era : Economic volatility

A big tech sell-off. US Federal Reserve rate hikes. Growing recession concerns. Geopolitical turmoil. It’s all starting to feel a lot like the early 2000s where a teaser oil cycle from 1999-2002 preceded the 2004-2008 super cycle. As always, history is more likely to rhyme than repeat and there are both striking similarities and big differences between the current environment and 20 years ago. The differences skew toward the current environment looking more favorable for oil prices and oil equities vis-a-vis the early 2000s.

With that said, traditional energy is not immune from recession, with downside risk to both oil prices and oil equities likely in the event recession does materialize. However, 20 years ago, it was not at all obvious or expected that a new super-cycle was around the corner. This time around, the combination of limited enthusiasm for a major CAPEX cycle from anyone (investors, industry, policy makers, politicians), the long-term negative outlook for Russia oil supply, and the fact that oil demand ex-recession is not on-track to rollover anywhere near as quickly as climate die-hards would lead you to believe, all point to an eventual resilience to traditional energy versus broader indices in the event recession does materialize.

Moreover, the better historical analog is almost certainly the stagflationary 1970s than the booming global growth of the 2000s. Oil prices did not trade freely in the 1970s (pre-NYMEX) and only the names of the integrated oils would likely be recognizable to most current investors. But the very concept of stagflation (stagnant economic growth but high inflation) comes from that time period. Arab Oil embargoes seem unlikely. But Russia turning into a pariah state is likely just as disruptive if not more so.

A look back at major corrections over the past 30 years

Asia Financial Crisis - 1997-1998

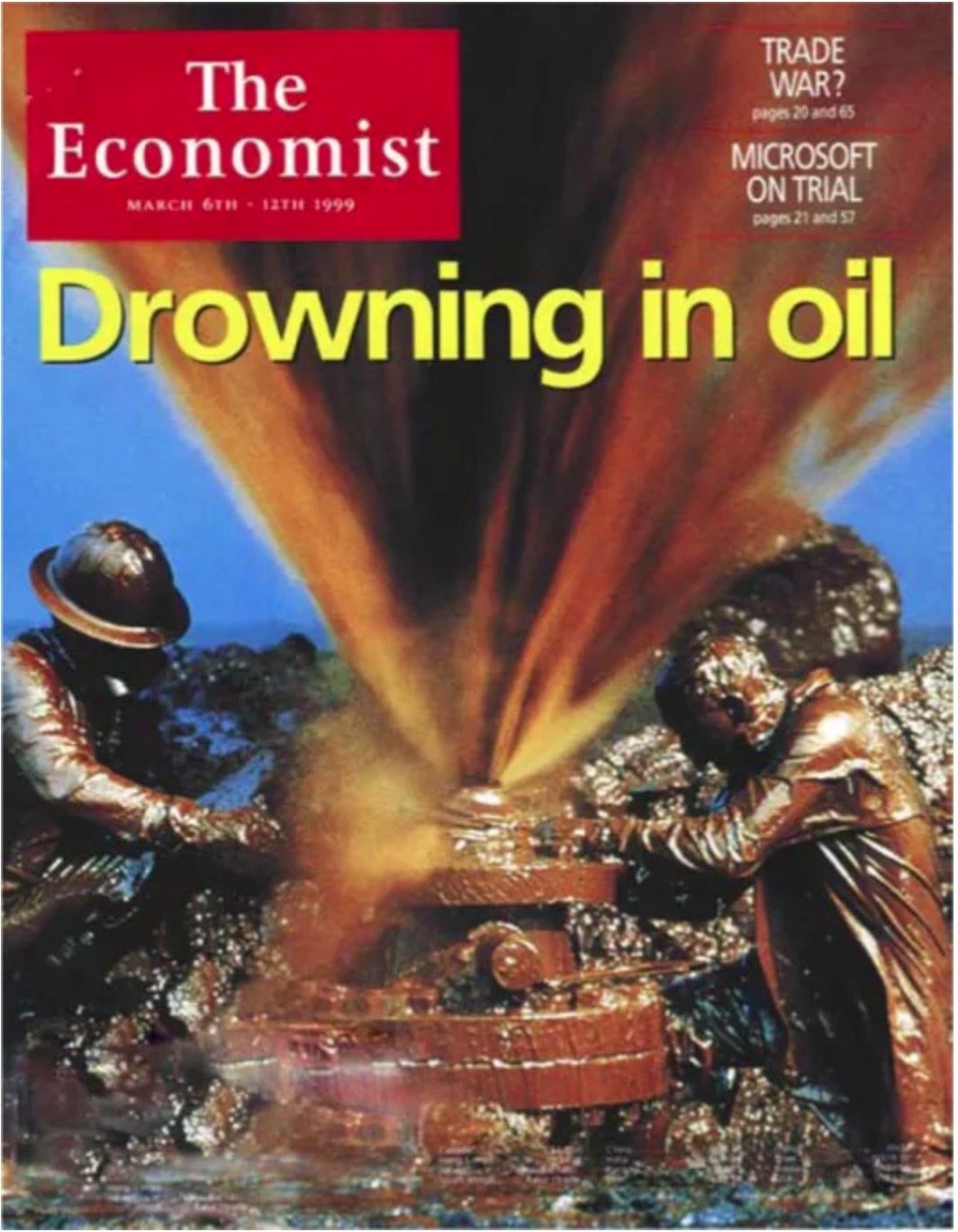

The Asia Financial Crisis started with the crash of the Thai Bhat in June 1997 and ultimately spread to what were then the faster growing Asia economies known as the “Asian Tigers”. With the region emerging as an important oil demand growth driver, the Asian economic downturn coupled with an ill-timed OPEC production increase (i.e., price war) led to oil falling below $11/bbl in December 1998. The ultimate sign of the trough was the March 4, 1999 article in The Economist (at the time, an influential publication), Drowning in Oil. With hindsight, this was the structural cycle bottom for crude oil and oil equities, with the sector experiencing a massive rally to its 2008 peak.

Exhibit 1 shows that the S&P Energy Index was essentially flat in absolute terms from the start of the crisis to the point that WTI spot oil hit bottom. Energy, however, badly trailed the S&P 500 and Nasdaq Composite.

Internet Bubble - 2000-2002

Most Super-Spiked readers will fondly remember the glory days of the so-called “dot com” era where creation of a website on The Internet qualified as ground-breaking corporate activity (not a joke). It’s recent enough that I won’t belabor the section. The ultimate highlight of this era was the January 31, 2000 Super Bowl ad by Pets.com, though some might argue the press conference for the AOL-Time Warner merger was the more iconic moment. In my view, the bursting of the Internet Bubble, corresponding Fed rate hikes, and subsequent recession is the most similar period within the last 25 years to what we are experiencing today. Especially since the earlier period transitioned to the Super-Spike era of 2004-2014.

Using the peak and trough of the Nasdaq Composite, the energy sector fell in absolute terms but meaningfully outperformed Nasdaq and the S&P; oil prices were essentially unchanged over the period (Exhibit 2).

Great Financial Crisis - 2007-2009

Memories will be fresh even among younger Super-Spiked readers. This of course was a Financial Crisis first and foremost. While the $145/bbl July 2008 oil price peak still stands as the highest nominal oil price on record—and was quickly followed by a 77% collapse to a $34 low in December 2008—the fast rebound back to a $100+ oil price environment over 2011-2014 suggests this major event did not mark the end of the Super-Spike era.

Exhibit 3 shows that the Financials sector (XLF) collapse during the GFC was comparable to Tech’s implosion during the Internet Bubble. While Energy technically outperformed the S&P and Nasdaq by 10%-15% using these dates, it still fell by a meaningful 41% in absolute terms. If instead the peak and trough of crude oil were used (Exhibit 4), Energy lagged the S&P and Nasdaq by about 10%. I would conclude that Energy did about the same as the broader indices during the GFC sell-off.

COVID - 2020

Notably, the energy sell-off during the initial COVID wave in Spring 2020 was actually the harshest on record (Exhibit 5). Worse than 2008 or any other crisis environment. I believe there are several reasons for the particularly poor performance:

The decline in oil demand was the most severe on record by many orders of magnitude; whereas oil demand might fall by 1-2 million b/d for a quarter or two in prior recessions, it fell an unimaginable 20+ mn b/d in Spring 2020.

The downturn came in year 14 of a deterioration in returns on capital for the sector and at a time that balance sheet health was mediocre-to-poor for most companies.

The latest cries that it was “End of the Age of Oil” were gaining mainstream acceptance.

I would suggest that the super-severe nature of this sell-off, the full extent of which I do not believe was justified based on long-term fundamentals, suggests that a decent portion of the bounce-back we have had in 2021 and 2022 is merely a much-needed normalization. This would be a point of debate for those more bearish on energy. I would simply say that a long-term 0% ROCE — as evidenced over 2011-2020 — was never going to be sustainable. A commodity sector like oil that has an expected 1% p.a. volume growth rate and an inherent decline curve that requires year-in, year-out investment should earn at least an 8%-10% “cost of capital” return over the long run. When you throw in all the ESG and left-of-center political and policy hurdles, normalized ROCE likely needs to be 12%+ to attract investment.

Current sell-off

The current market sell-off, where the Nasdaq is down 29% from its peak and the S&P 500 is down 17% (from the Nasdaq peak date), is not like any other. Energy stocks are up a stunning 50%. The disconnect is likely raising concerns from investors that Energy is due for a correction. That may well be true. But as I will discuss in the next section, there is a large reversion to the mean and reversal of prior excessive pessimism that I think accounts for much of the rally to date. The real bull market I suspect has barely begun.

What is the takeaway from past crises? Energy is not immune from recession but context matters

Not all sell-offs are created equal and not all economic downturns impact Energy in the same way as we can see from the above performant tables.

Some thoughts:

Where Energy is in the underlying structural ROCE cycle matters greatly. The COVID sell-off came at the end of a 15 year ROCE downturn. EVERYONE was absolutely done with traditional energy, resulting in particularly bad performance the aftereffects of which we are still seeing to this day.

The driver of the downturn or crisis matters. For example, Energy rebounded quickly from the Great Financial Crisis as supply/demand/spare capacity was ultimately still tight, the bursting of the Housing/Financials bubble wasn’t really an Energy issue, and we were otherwise in the middle of the 2004-2014 Super-Spike era. During the Asia Financial Crisis, energy performed worse as it was somewhat more uniquely exposed to those economies weakening vis-a-vis other S&P 500 sectors.

Where are we today?

In my view, we are just starting year 2 of a potentially decade-plus long ROCE super-cycle period.

Sector balance sheets have been repaired.

OPEC appears to be out of spare capacity.

Russia, a Top 3 crude oil producer, is in the process of turning into a pariah state, suggesting long-term downside risk to its oil production.

There is still a striking lack of any interest in a major new CAPEX cycle—traditional investors, ESG investors, climate activists, and left-of-center politicians that are currently in power in the key growth areas of USA and Canada are all against oil supply growth.

There is no evidence that the long-term relationship between oil demand growth and GDP growth has changed. Yes, a recession would by definition negatively impact oil demand. But the idea that oil demand was nearing a peak in a normal global GDP environment does not have supportive evidence.

Global policy and political elites continue to believe we are on the cusp of an imminent energy transition away from crude oil that does not require “long term” investments to be supported with sensible policies.

Other energy commodities are similarly tight.

Without adequate energy supply, economic growth will be forced lower. Without future energy supply CAPEX, this process is likely to be repeated on a somewhat regular basis over the remainder of this decade.

Notable Energy and Tech sentiment peaks and troughs

1999 (oil trough): Drowning in Oil, The Economist. An all-time classic magazine cover at a time The Economist was at the peak of its powers as an influential media organization. In fact, we were about to be starved for oil, which rallied from the $11/bbl late 1998 low to $145/bbl over the next decade.

2001 (tech peak): Pets.com Super Bowl ad. A bit like ARKK in the present, we all knew this was a sign of the top at the time. Still, internet euphoria drove the entire tech sector to incredible heights before a massive correction. If you really thought Pets.com was not real, you also needed to be skeptical of regular Tech stock valuations.

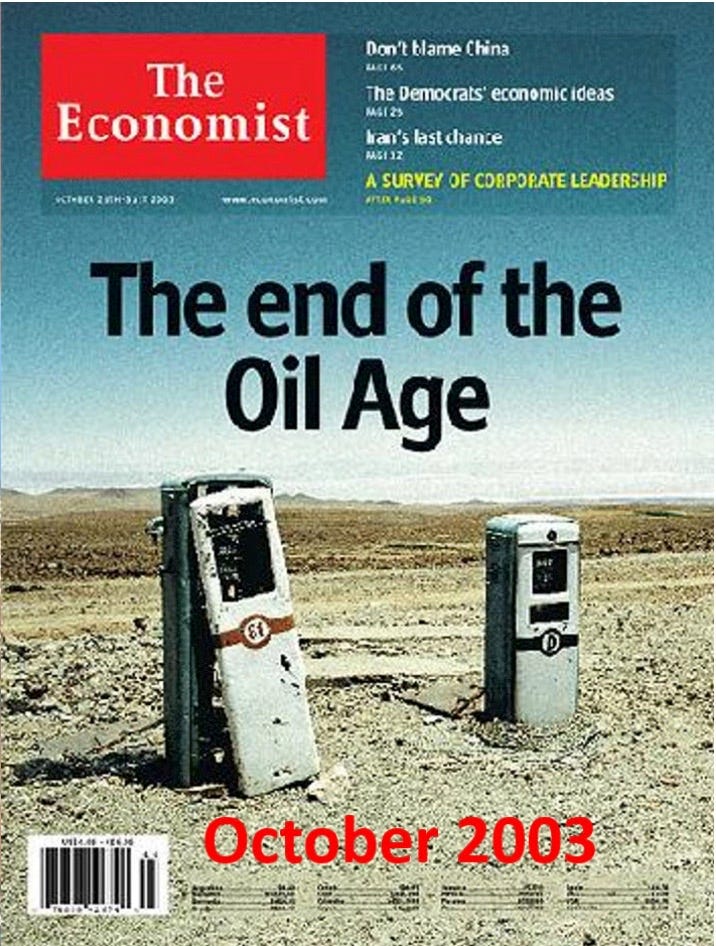

2003 (oil trough): The End of the Oil Age, The Economist. I am not trying to pick on The Economist. And kudos to them that the magazine covers are memorable. This was not the first and wouldn’t be the last time “The end of the Oil Age” was forecast. The Economist is far from being alone in incorrectly making this call.

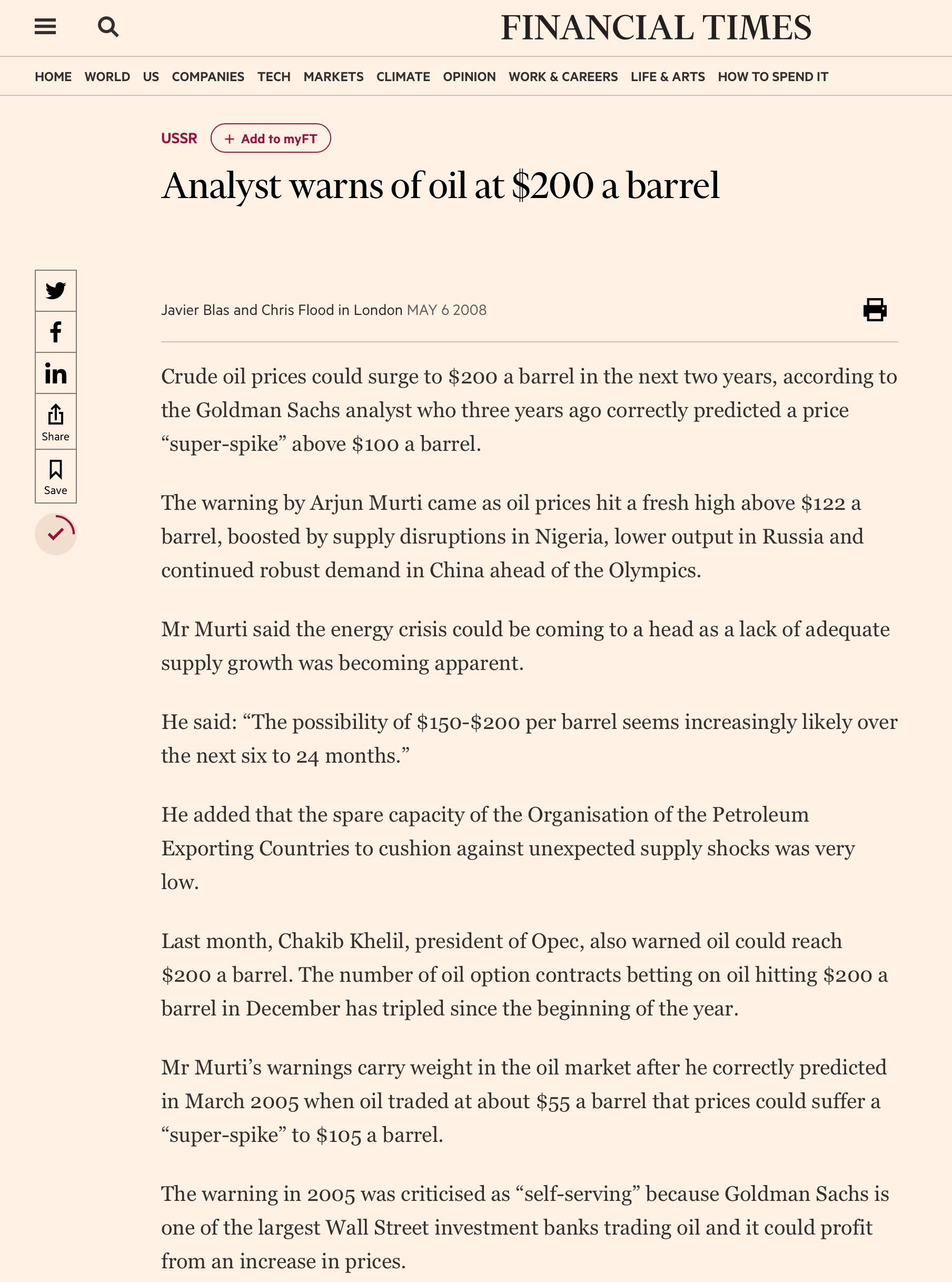

2008 (nominal oil peak): Goldman Sachs capital markets professional: “Welcome to The Jeff and Arjun Show”, São Paolo, Brazil, July 2008. While the mainstream media rarely accurately depicted our commodity calls, this one is on me as I should no longer have been surprised at how the call would be received. And, to be clear, I should not have doubled down in Spring 2008. My visit to Brazil with my former colleague jumps out as The Peak. (I should also confirm that the FT article shown below accurately reflected what I wrote; Javier Blas is now one of my favorite commodity journalists/writers and it is not surprising he accurately reported my call.)

2014 (end of Super-Spike Era): Bloomberg headline: “Goldman’s Super-Spike analyst hangs it up.” The idea of remaining a publishing analyst AND a member of Goldman research management in a post-oil bull market world was not something I aspired to do. Retiring as a partner at Goldman and spending more time with my then middle-school-aged children is one of the best decisions I have ever made. The foregone partner-level compensation was a low price to pay for my freedom and family memories. Taking a break from being a publishing analyst during the lean years has also been good for my mental and physical health as well as my golf game. It looks like Bloomberg’s web archive has changed the headline that I remember. And the Bloomberg retirement headline in February 2014 preceded my official stopping of active coverage in June 2014, a good five months before the fateful Thanksgiving 2014 OPEC meeting that crashed oil from the $100/bbl range to what would settle out at around $50/bbl for the next half decade plus.

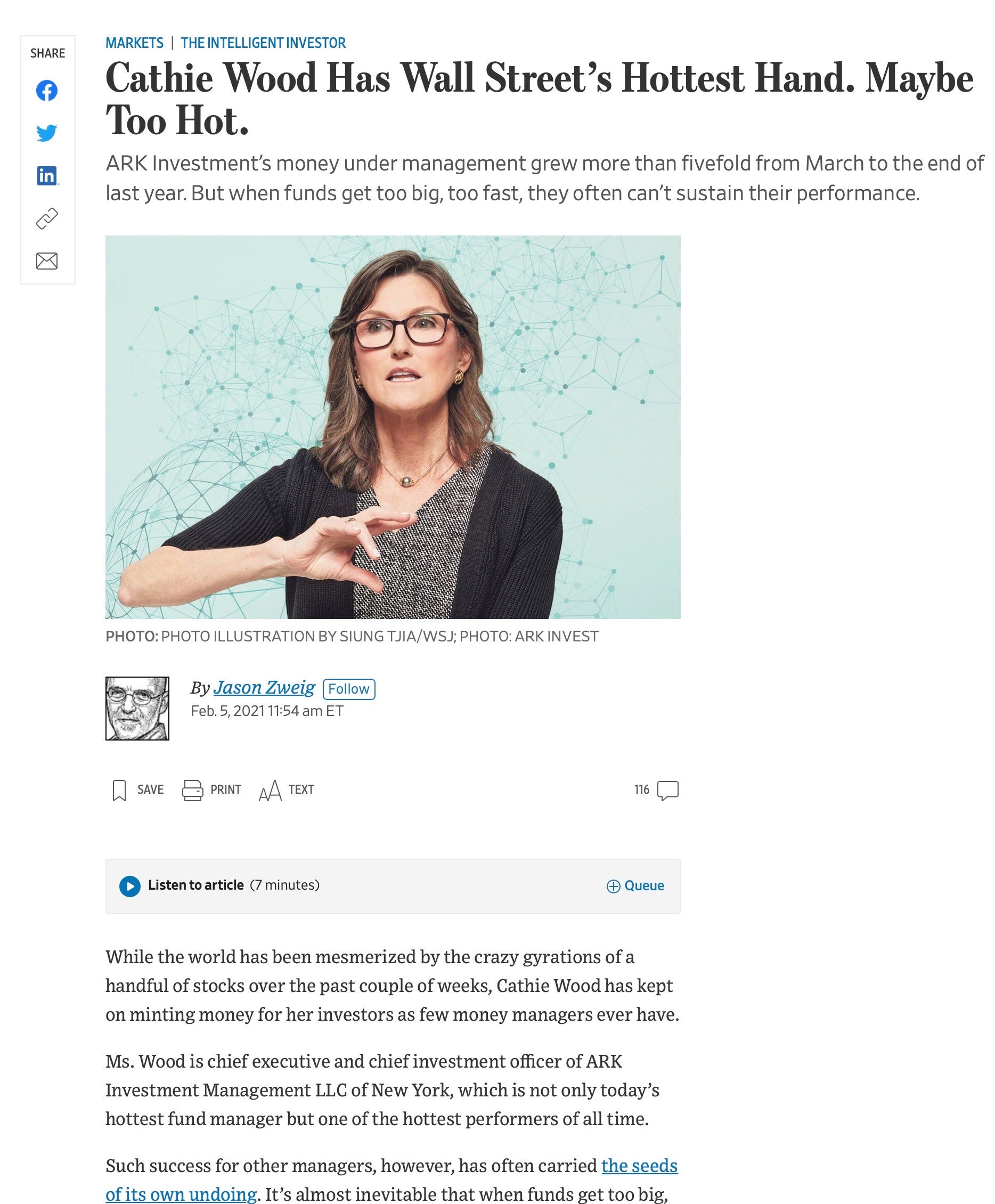

2021 (tech peak): ARKK peaks at $159.70 on 2/16/21. I will note that a Cathie Wood Google search for the second half of 2020 through February 2021 yielded a mixed bag of support versus skepticism. Even this Wall Street Journal article written just 11 days before ARKK peaked expresses uncertainty on the sustainability of her style. I suspect the difference is that the ARKK’s success was not a function of traditional, “mainstream” excessive enthusiasm but was more driven by the retail, meme stock crowd that uses newer media sources and communities. I probably should have done a Reddit or TikTok search instead. ARKK is a modern, more sophisticated version of Pets.com. We all knew ARKK wasn’t sustainable. But the broader Tech sector was still driven to incredible heights. If you didn’t like ARKK, you shouldn’t have liked other Tech stock valuations.

2021 (oil sentiment trough): IEA Net Zero by 2050 published on 5/17/21. Perhaps no publication better exemplifies the disconnect between global elites and the reality the rest of world faces than the International Energy Agency’s (IEA) Net Zero by 2050 report. To be clear, the IEA produces high-quality historical oil/supply demand data. There are many excellent professionals that contribute to the IEA and whose analysis and views I value. My critique is with the editorial direction its photogenic leader has taken in effectively promoting “climate only” ideology.

There is no trading call implied in this post

I know that some of you will wonder if my recession talk and energy not being immune is some sort of not-so-subtle message that I think a pullback is imminent. I am already on record of expecting a “super vol” environment featuring both sharp rallies and regular selloffs. As for the short-term, let me say this unequivocally: I am not a short-term trader and am not making a trading call in this post. Rather, my intention is to provide a framework for how to think about inevitable energy sector market volatility and what it may mean, or not mean, about the sector’s long-term prospects. I believe that when we reach 2030, investors and analysts will look back and find traditional energy performed very well versus broader market indices during the 2020s. The structural energy cycles are long-term in nature. This one started in 2021. We are barely in Year 2 of what I think will be a very good decade for traditional energy.

⚡️ On a personal note…

Vying for Attention in an Internet World. That was the title of my launch report at Goldman Sachs. In the second half of the 1990s, as the tech bubble was inflating, I specifically remember going up to 50th floor at One New York Plaza on December 8, 1999—my major oil coverage launch date at Goldman Sachs—and running into a fellow equity research analyst from the tech sector.

Me (Vice President, earning a respectable living by non-Wall Street standards): Hi, my name is Arjun.

Hot shot tech analyst (title irrelevant, comp was super high and undoubtedly many multiples of mine): Nice to meet you Arjun. My name is “Maverick” (not his actual name). I cover some obscure but super-hot tech sub-sector that trades at 25 times eyeballs. What do you cover?

Me: I just launched coverage of the US integrated oils.

Tech analyst: (Sighing) Oh, I am sorry to hear that. (that is a direct quote that I have never forgotten; he was not joking)

Me: (silently thinking and looking quizzically at him: Exxon’s like always a Top 3 S&P 500 stock. At all times, everyone always cares about the oil price. I am now going to be the Goldman Sachs MAJOR OILS analyst. Your sector trades on eyeballs. I think I’ll be fine.)

Hot shot tech analyst: OK then. Good luck and good bye.

Needless to say, hot shot did not even make it to the NASDAQ peak at Goldman. I lasted another 15 years. In the late 1990s, the energy sector, while not being hot, still mattered. I am grateful to all my former colleagues in Sales & Trading who helped my launch get to off to a decent start despite energy being decidedly out of favor and not trading on eyeballs.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Regards,

Arjun

P.S. There will be no Super-Spiked published over Memorial Day Weekend. Welcome to summer!

Hello Arjun, I look forward to a new Super Spiked and always read it first before anything else that day. It's top priority.

I know that you are not making trading calls, I fully acknowledge that, so can I ask about what you think the rough floor and ceiling on crude prices will be during this superspike period? I.e. demand destruction we seem to have reached at ($120 crude + crack spread of $40 = ~$160) at the pump during the March 2022 and June 2022 peaks, is that ~$160 range about the ceiling on prices for this period? And the shut-in floor, what price range? Again, I'm not looking for a specific prediction but just the general range you see prices gyrating within. Any clarification is appreciated.

Best,

J

I enjoyed this article so much that I went back in time and bought tons of XOM on margin at $34 right before the 2020 election. Actually didn't have to go back in time, actually did it. It's so refreshing to hear some common sense from someone who was at the top and not just little people like myself. How anyone could think oil is going to disappear any time soon boggles the mind. So grateful to the guy on seeking alpha who sent me a link to this post and I'm now a subscriber.