Transitioning Corporate and Investor Risk Taking: Q&A and Clarifications

The Energy Transition Needs to Transition

Our last two issues of Super-Spiked (here and here) focused on the super theme that "The Energy Transition Needs to Transition" to one centered on figuring out how to meet the energy needs of the other 7 billion people on Earth that do not live in the United States, Europe, Canada, or Japan. This week we apply that lens of the "energy transition needs to transition" to one of our favorite topics: helping publicly-traded energy companies think through how to achieve one of three good long-term outcomes while avoiding the two bad ones (discussed in more detail here).

As a reminder, the three good long-term outcomes are:

Outperform the S&P 500 (or corresponding major benchmark if not US-based) over 5, 10, and 20 year increments.

Sell or merge with another company.

Liquidate and return all cash back to shareholders.

The two bad outcomes are:

Purgatory: Fade to “living dead” status where the company trails the S&P 500 and becomes irrelevant to most investors, though otherwise remains viable.

Bankruptcy and the elimination of equity value.

We all know last decade was terrible for traditional energy in terms of poor (and declining) profitability, rising debt levels, and a shrinking S&P 500 weighting. Since the Fall 2020 trough, all three metrics have improved dramatically even taking into account the pullback seen year-to-date. Yet investors have not fully re-embraced the sector for a variety of reasons including short-term recession concerns, long-term "transition" demand uncertainty, and fears that allowing any amount of risk taking is a slippery slope back to the bad ole days of over-spending for growth without adequate full-cycle profitability.

The catch-22 of "don't you dare spend even though your inventory running room won't sustain your business" will reconcile in coming years in one of two primary ways: (1) companies will make acquisitions to extend the runway (something that has started) or (2) companies will enter liquidation mode. To be sure, #2 is an option some should consider, even if it is essentially untested in publicly equity markets. An in between option that could work well for some management teams would be to alternate between growth and shrinkage. Active portfolio management as a strategy has helped many companies improve themselves, though it's usually treated as "one time" in nature, after which a company is presumably back on track to being a viable going concern.

Q. With profitability and balance sheet health much improved, what needs to transition most going forward?

A. Many companies are in need of extending the runway (i.e., adding projects, assets, acreage) by which advantaged returns can be generated.

Q. What is standing in the way?

A. Extreme risk aversion by investors, boards, and management teams after last decade's debacle.

Q. How can risk taking increase without ruining the progress that has been made on returns and balance sheet health?

A. Risk taking is unavoidable. It is not possible to sustain competitive profitability over the long run without taking risk. Pretending otherwise is simply delaying the inevitable.

Q. Why aren't investors seemingly more excited about companies that are generating better profitability and appear more committed than ever to returning a decent amount of cash back to investors?

A. Try this as an exercise: Go name-by-name through the universe of publicly-traded traditional energy companies. How many would you say have (1) a senior management team that you trust with capital allocation; (2) an opportunity set that is differentiated from peers and can generate competitive profitability over a "decadal" type time frame; or (3) a senior management team and board that recognize inventory or strategy limitations and are willing to liquidate. To be clear, a company with an "acquisition and exploitation" mindset might well meet the first two criteria—perhaps the modern version of the old XTO Energy strategy from the 2000s or Apache from the 1990s.

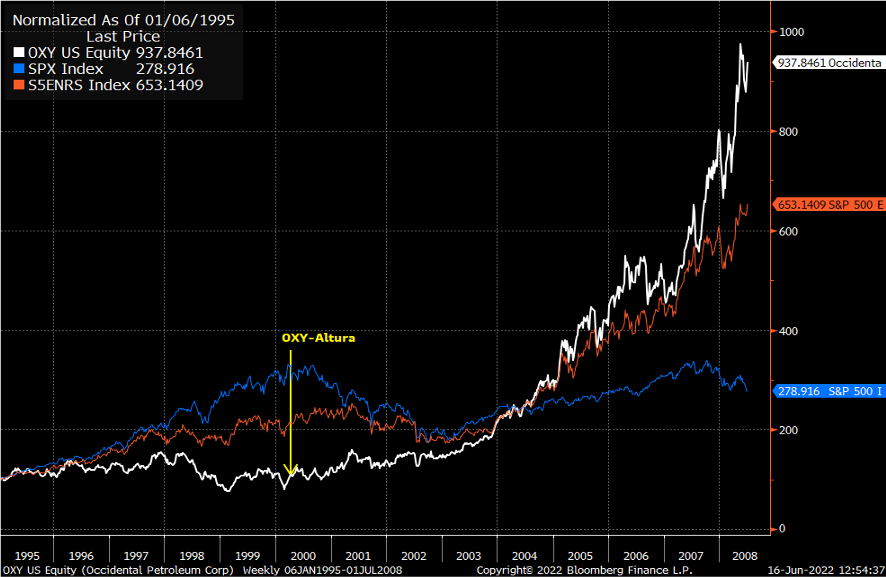

We would also note that for companies that may not check boxes #1 or #2, it is possible to change investor views based on actions taken. OXY in the 1990s, which I have discussed in previous posts (here and here), is perhaps the best example in my career where investors flipped from being understandably distrustful of capital allocation to the company becoming a sector leader (Exhibit 1).

Exhibit 1: OXY shares badly lagged the sector and S&P 500 in the 1990s, with the Altura acquisition ultimately contributing to a massive turnaround the next decade

Source: Bloomberg

Q. Many are not as confident as Super-Spiked is that oil demand will continue to grow for at least another decade (if not longer) and are similarly concerned that natural gas demand is primarily a rest of world LNG (liquefied natural gas) opportunity that is beyond the purview of all but the largest companies. Shouldn't companies simply continue to emphasize capital return strategies over "risk taking" given the uncertainty?

A #1. There are certainly companies that likely should not engage in risk taking. Companies with limited resource bases or opportunity sets might well be better off engaging in consolidation that can drive G&A and related savings that can help boost shareholder distributions. The discounted valuations we see for many smaller companies, especially in the traditional upstream sector, may well reflect concerns about the future strategic direction of companies with limited opportunity sets. We expect M&A activity to increase.

A #2. We have now repeated this point many times: shareholder distributions will never be sustainable without some amount of risk taking.

Q. Isn't the Inflation Reduction Act and similar legislation in other countries a sign that growth in new energy technologies will in some coming decade displace oil, natural gas, and coal?

A. That very much remains to be seen. The energy needs of the other 7 billion people on Earth are massive. We will need all forms of energy supply going forward. The mere existence of large government subsidies for many new technologies does not guarantee that any specific technology will scale up to the point it can prove its mixture of availability, affordability, and geopolitical security will prove better than oil, natural gas, or coal. Our base-case outlook is that crude oil demand will grow at least into the mid-2030s, natural gas demand will grow for the foreseeable future (i.e., beyond 2040), and even coal demand likely grows for at least this decade if not longer.

Q. How can undue uncertainty over short- and long-term demand including the displacement potential (or not) of new energy technologies benefit traditional energy companies?

A #1. Very few investors today are demanding a production growth forecast; in fact, just the opposite. There is an ability to buy and sell assets and to invest in conventional or offshore opportunities that will have lumpier production growth profiles than what was expected during the era of shale ascendancy.

A #2. The goal is to outperform on a total return basis a relevant index (usually the S&P 500 for US-based energy companies). It is not about trying to get a high current cash flow multiple, which too many management teams seem to spend a lot of time contemplating. As such, areas of opportunity do not have to be limited to the popular, "safe" choices which today seems to mean Permian or other US shale acreage.

A #3. The flip side of a high cost of capital for individual companies (i.e., low cash flow multiple) is that capital formation and competition is similarly low (versus history).

Q. Which traditional energy companies are best positioned to take advantage of the growing split between the climate obsessed western world (Western Europe, US, Canada) and the energy supply needs of the rest of the world?

A. Companies that maintained an international presence. The shale boom of the past 10-15 years drove many companies to divest or otherwise let atrophy international divisions. Companies that have maintained an international presence will be better positioned to evaluate international investment opportunities.

Q. Should traditional companies invest in new energy technologies as a means of differentiation?

A. In some cases the answer may be "yes" and for many others the answer will almost certainly be "no.s" In some respects, new energy technologies are the modern exploration business. The logical extension to core businesses have the potential to make at least some sense at this time, something we are seeing with a handful of upstream companies engaged in CCUS (carbon capture, utilization, and storage) and many downstream companies via renewable fuels expansions.

Q. What is the most differentiated move a company can make?

A. Expansion in really any area that is not US shale would be differentiated today. Right now adding shale acreage is not differentiated though it can obviously make sense for some companies based on location, price paid, etc. To be clear, nothing in this post should be construed as anti-shale. The point is simply that we no longer believe it needs to be the only game in town as especially upstream-oriented companies think through corporate strategy.

It is possible that select new energy technology investments could be differentiating for traditional energy companies. That said, investors will understandably want to understand the competitive advantage a traditional company brings to the area, as well as the risk/reward to achieving unsubsidized commercial scale.

Q. What are historical examples of management teams that bucked the trend and achieved significant outperformance?

A. Three example from the first half of my career (1992-2007)

1. Tom O'Malley at Tosco (buying refineries for a fraction of replacement cost)

2. Ray Irani and Steven Chazen turning around Occidental Petroleum (catalyzed by the Altura Energy acquisition in the Permian Basin)

3. Bob Simpson and team via XTO Energy (acquire and exploit US onshore/shale)

We have discussed each of these examples previously. What they have in common is the management teams went against the grain with the preferred approach by most other companies and, initially, investors. A stick with the pack philosophy is appropriate for wolves. For companies, successful differentiation can unlock differential outperformance.

Q. Who today is willing to buck the trend and expand outside of US shale?

A. We don't know the answer to this question. But if history is any guide, there will be a narrative-changing transaction that jumps out and is ultimately well received by investors.

⚡️On a Personal Note: Sedona and St Andrews

Since un-retiring to Veriten in March, my travel schedule has picked up considerably. The first twelve weeks have included multiday trips to New York, Houston, Washington D.C., New York again, Houston trip #2, Las Vegas, Houston trip #3, and next week will be Houston trip #4. (Yes, New York counts even though I live in this area; morning-through-dinner meeting schedules over multiple, consecutive days did not occur over the previous 8 years.)

But when my college junior daughter asked what we were doing for Spring Break and said she would join wherever we were going, we created a trip to Sedona. We had no prior plans, but she asked so we made some. Good decision #1. When my college sophomore son asked which days I would be coming out for my annual spring golf visit to St Andrews, I similarly did not have an intention to go this year. But he asked, so I squeezed in a long weekend trip to Scotland between Houston visits. Good decision #2.

Lundin Golf Club in Lundin Links, Fife

Source: Super-Spiked.

⛳️ The Un-retirement Blog: Episode 3

Traveling with Veriten is a million times better than my memories of traveling as a Goldman analyst, especially once the kids were born. I loved interacting with institutional investors. It was really the core purpose of being a GS analyst...help investors think through the energy sector. But there were times you'd be counting down the minutes during the 28th meeting in the midst of a week long trip at 9 pm on a Wednesday, hoping to catch the last inning of the deciding Yankees-A's Game 5. And it was pure misery being away from the kids during their pre-teen years.

By comparison, hanging out at The Ion with the great Veriten team is energizing. And I think I can safely say that I would not have previously been able to attend The World Oilman's Poker Tournament in Las Vegas, a great networking event of mostly private oil & gas executives and related participants. So yes, it's a lot of travel, but it's not the same. It's much more enjoyable.

Finally, I have an important update on progress toward my 2023 golf goals. The core golf season in the US northeast typically starts in April and runs solidly through October. In Episode 2 of The Un-retirement Blog, I expressed concern about missing my 60 round target established in January. To be sure, the season started slow but has since picked up. Including 9 hole days (i.e., played a full nine holes on two different days for a completed 18), I have played 17 rounds through May 12. My GHIN has backed up from a 7.6 low to 8.9 currently. I project it will rise to 10 in the coming weeks (as a few more low rounds from the end of last year roll off), after which I will attempt to get back to single digits.

In terms of courses played, I have enjoyed work trips to the Wynn Golf Club in Las Vegas and The Club at Carlton Woods for a pro-am ahead of The Chevron Championship, and a Spring Break visit to Seven Canyons in Sedona. Two weeks ago I played at an MGA (Metropolitan Golf Association) charity outing at Winged Foot. By the time this post is published, I will have played Baltusrol.

But nothing in the world compares to links golf in the Kingdom of Fife. The Castle Course, Lundin Golf Club, Leven Links, and The Eden Course were on the docket last weekend (Eden replaced Crail Balcomie Links where we were fogged out). Leven Links is always a fun stop after an overnight flight to EDI on the way to St Andrews. At Castle, I am pretty proud to have gutted out a respectable round on a very challenging course during a steady rain. At Lundin, a few mental lapses cost me my first sub-80 round of the year, but I came away quite encouraged about being able to get back on-track. No surprise: putting and short game practice time is needed.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.

Arjun,

1. Congratulations on picking up the pace in getting in rounds of golf.

2. Glad to hear your “unretirement” is enjoyable and worth the travel. Especially when you can combine fun and work.

3. Would whole heartedly applaud the oil & gas companies either taking themselves private or merging. Merging the right companies would allow them to gain synergies and extend the runway of proven reserves. Should enable the right companies merge it would lower their break even cost per barrel even further e.g XOM buys PXD.

I don’t see as big a reduction in cost related to going private, but for some it would allow them to increase their dividends by shedding certain costs.

4. What about the right majors buying companies who are in involved in carbon capture e.g. AMTX or others. The majority don’t have major market caps and would benefit under the umbrella of a larger company. AMTX needs to either sell its major profit source or gain larger carbon credits to grow.

Fully agree with James Robertson that the majority of these companies will not move unless an event causes this to occur or you talk them into it.

Very interesting point of view. What about #4, pivoting to alternate complimentary business? e.g. BHP , a mining company, got into oil and gas. Oil companies getting into lithium